Why Holding Stacks Decide Whether Wealth Survives Shocks

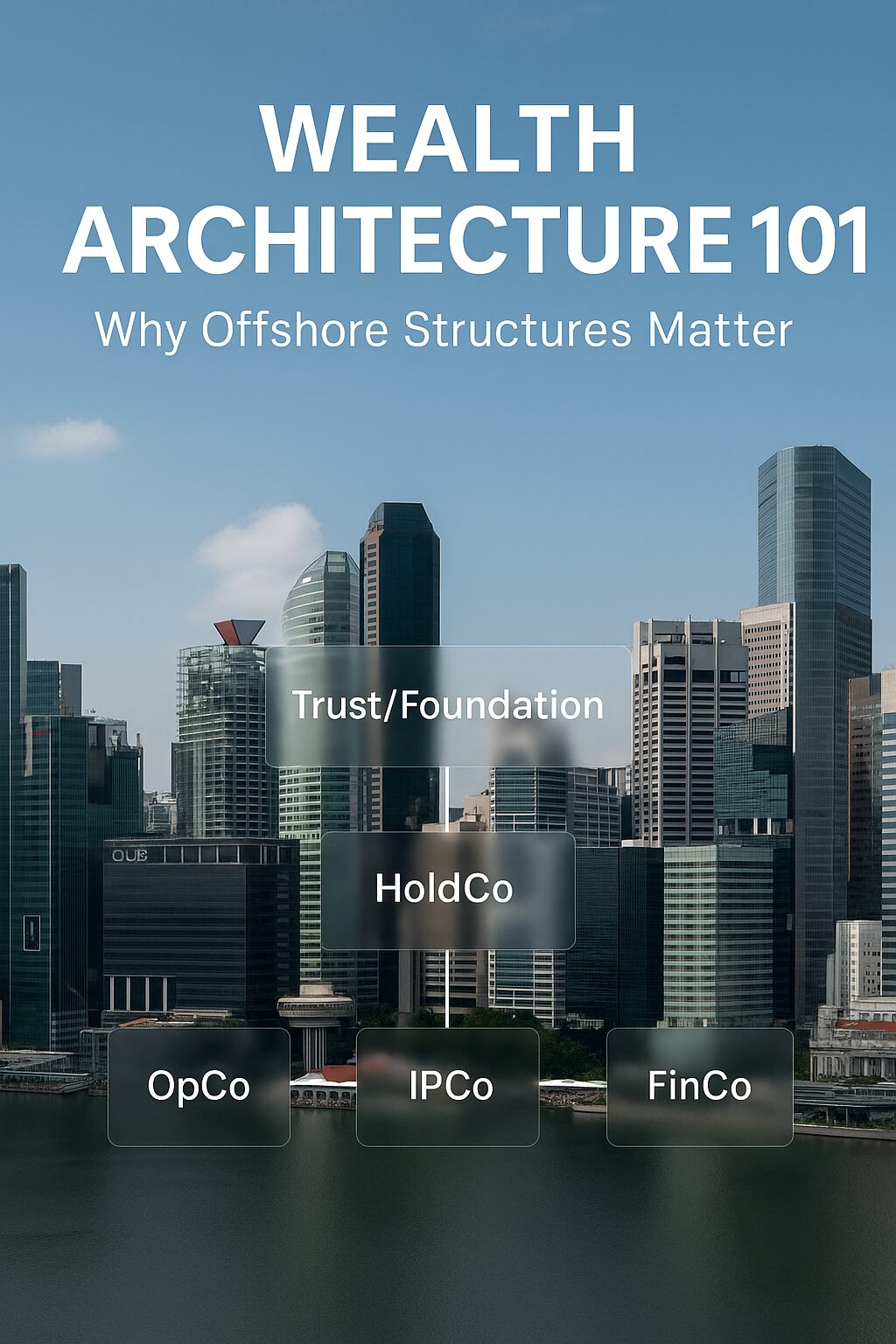

In global wealth planning, the most overlooked truth is simple: structure beats size. A fortune without fences is fragile; a moderate portfolio with disciplined ring-fencing often survives crises intact. Holding company stacks — composed of parent HoldCos, operating subsidiaries, IP companies, financial hubs, and project SPVs — are the architecture that makes asset protection real.

This article will show how to design and operate a holding stack that withstands lawsuits, market shocks, regulatory scrutiny, and even family disputes. We’ll map the core building blocks, explain cashflow routing, show how to enforce arm’s-length intercompany agreements, and detail diagnostics you can use to measure ring-fence strength.

Main Body

1) Anatomy of a Holding Stack

A resilient structure usually includes:

- HoldCo (Holding Company): Owns shares in operating and asset entities. Minimal liabilities.

- OpCo (Operating Company): Interfaces with customers, hires staff, carries most external risk.

- IPCo (Intellectual Property Company): Owns patents, trademarks, software, brands; licenses IP to OpCo.

- FinCo (Financial Company): Runs treasury, custody, hedging, financing, intercompany loans.

- SPVs (Special Purpose Vehicles): Each project, JV, or real estate asset in its own box.

The purpose is segregation. If OpCo is sued, IPCo and FinCo remain untouched. If one SPV fails, the others live on.

2) Why Ring-Fencing Works

Ring-fencing is the deliberate isolation of risks and assets so shocks cannot spread.

- Legal segregation: Each entity has its own legal personality.

- Financial segregation: Separate accounts, contracts, and invoices.

- Operational segregation: Different boards and governance cycles.

Example: If OpCo faces product liability litigation, plaintiffs cannot automatically seize IPCo-owned trademarks or FinCo-held treasury.

Key principle: Protection only works when paper and practice match. Empty boxes with no invoices, no minutes, and commingled funds will collapse under scrutiny.

3) Intercompany Agreements — The Arteries of the Stack

Each relationship must be formalized with contracts:

- IP License Agreement: IPCo licenses patents/brands/software to OpCo for royalties.

- Service Agreement: HoldCo or FinCo provides management/treasury/HR services; OpCo pays fees.

- Cost-Sharing Agreement: Shared resources (IT, office, staff) allocated by formula.

- Dividend Policy: Rules for when and how subsidiaries pay dividends to HoldCo.

- Loan Agreements: FinCo extends credit to SPVs or OpCos, with terms.

Why they matter: Regulators and courts look for arm’s-length behavior. If cash moves without contracts, risk leaks.

4) Cashflow Engineering

Core routes:

- Royalties (OpCo → IPCo)

- Dividends (OpCo/SPVs → HoldCo)

- Management fees (OpCo ↔ HoldCo/FinCo)

- Loan repayments (SPVs → FinCo)

- Wages/board fees (to humans)

Best practices:

- Document every flow with contracts, invoices, and approvals.

- Schedule flows (monthly royalties, quarterly dividends).

- Match currencies where possible to reduce FX leakage.

- Reconcile accounts monthly.

5) Jurisdiction Mix — Diversification as a Defense

Avoid “all eggs in one jurisdiction.”

- HoldCo: Often in treaty-rich, stable jurisdictions (e.g., Netherlands, Luxembourg, Singapore).

- OpCo: In customer markets.

- IPCo: In IP-friendly, royalty-efficient jurisdictions (Ireland, Switzerland).

- FinCo: In financial hubs (Luxembourg, Hong Kong).

- SPVs: In project-specific jurisdictions (Delaware for U.S. real estate, Cayman for JV).

Principle: Legal, tax, and banking risks should be geographically diversified.

6) KPIs of a Healthy Stack

- Contagion score: How many walls exist between external risks and core assets?

- Liquidity mobility: Can cash be upstreamed smoothly with approvals?

- FX efficiency: % of cash flows naturally matched in-currency.

- Governance cadence: Boards/councils meet on schedule with evidence.

- Compliance posture: All filings, audits, and registers are current.

7) 30-60-90 Day Holding Stack Implementation

First 30 days — Mapping & Incorporation:

- Draft entity map.

- Decide jurisdictions for each box.

- Incorporate HoldCo, IPCo, FinCo.

Next 30 days — Agreements & Accounts:

- Draft intercompany contracts.

- Open multi-currency accounts.

- Transfer IP to IPCo.

- Seed FinCo with treasury capital.

Final 30 days — Operationalize & Test:

- Issue first intercompany invoices.

- Approve and pay first royalties/dividends.

- Run a stress-test drill (OpCo litigation, FX freeze, SPV insolvency).

- Document responses and minutes.

8) Common Failure Modes

- Decorative SPVs: Formed but never capitalized, invoiced, or governed. Courts ignore them.

- Single-jurisdiction exposure: All entities in one country; local law changes wreck the whole stack.

- Paperless flows: Cash moved without contracts or invoices.

- Founder control everywhere: Same person as director in every box; no independence.

- Annual clean-up culture: Retroactive minutes, fake invoices.

9) Diagnostics Checklist

Ask these questions quarterly:

- Does each entity have separate accounts, contracts, and invoices?

- Are boards meeting and recording minutes?

- Is FX being managed purposefully or reactively?

- Are secondary banks/rails tested?

- Could a creditor in one SPV realistically reach IPCo or FinCo assets?

Conclusion — Holding Stacks as Engines of Resilience

Wealth endures when risks are quarantined and cash moves with discipline. A proper holding stack does three things:

- Isolates operations from intellectual property and treasury.

- Separates projects into SPVs so failure does not spread.

- Documents flows so protection survives audits and litigation.

This is not decoration; it is survival engineering. Entrepreneurs and families who respect the architecture enjoy continuity even in crisis. Those who treat entities as paperwork invite collapse when tested.

Case Studies (placed just above preview)

Success — Litigation Contained by SPV Structure

- Design: Developer used separate SPVs for each property; HoldCo only held shares.

- Shock: One property faced defect litigation.

- Outcome: Liability quarantined in one SPV; other projects continued.

- Lesson: One project, one box, one exit.

Success — IP Protected Through IPCo

- Design: Global brand parked trademarks in IPCo; royalties documented.

- Shock: OpCo sued for defective product.

- Outcome: IP untouched; brand leveraged for refinancing.

- Lesson: IP belongs in IPCo, not OpCo.

Failure — Paperless Intercompany Loans

- Design: FinCo advanced cash to OpCo without agreements.

- Shock: Tax audit.

- Outcome: Loan reclassified as taxable distribution; penalties applied.

- Lesson: Every flow needs paper.

Failure — All Entities in One Country

- Design: HoldCo, OpCo, IPCo all in one jurisdiction.

- Shock: Political instability; banking restrictions imposed.

- Outcome: Entire group trapped; liquidity frozen.

- Lesson: Jurisdiction diversification is not optional.

Next Article Preview

Banking & Multi-Currency Systems — Custody, Settlement, and Treasury Architecture

In the next article, we’ll dive into the plumbing of global wealth: multi-currency accounts, custody arrangements, settlement rails, and treasury SOPs. You’ll see how to design a multi-bucket system that reduces FX slippage, avoids payment freezes, and ensures liquidity even during banking shocks.