1. Introduction: Why One Income Stream Is Never Enough in 2025

Relying on a single paycheck in 2025 is financial suicide. With inflation, unstable job markets, and global crises becoming the norm, people who thrive financially are those who build systems—not just careers. This guide isn’t about “get rich quick” hacks. It’s about real, sustainable passive income streams that you can start today, regardless of your background.

2. What Is Real Passive Income? (Not What You Think)

Forget the myths. Passive income isn’t 100% hands-free. Real passive income means you build once, earn repeatedly. Whether it’s an eBook, a blog, or a monetized video, there’s always initial effort. But the goal is to reduce time-for-money dependence and let your content or capital do the work.

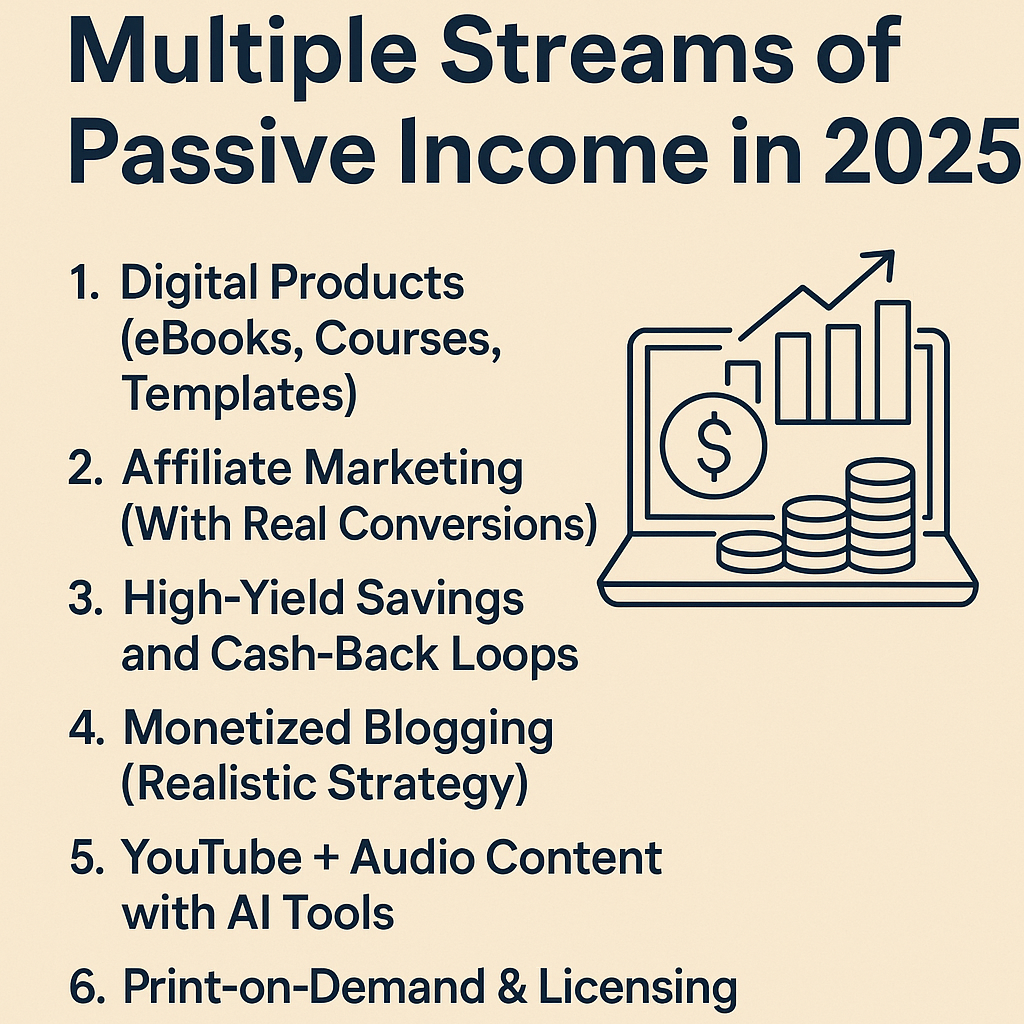

3. Stream 1: Digital Products (eBooks, Courses, Templates)

Creating digital products is one of the most scalable passive income models. Examples include:

- A $15 eBook that sells 50 copies a month = $750/month

- A Notion template that helps freelancers organize their tasks

- A mini-course on teaching Excel basics on Gumroad or Teachable

Tools to start:

- Canva (design)

- Gumroad (sell)

- Loom (recording)

- ChatGPT (drafting ideas)

Build once, automate sales, and you’ve built a 24/7 online store.

4. Stream 2: Affiliate Marketing (With Real Conversions)

Forget spammy links. The real game is trust-based recommendations.

Start by:

- Picking a niche you know well (travel, personal finance, etc.)

- Creating helpful content (blogs, YouTube, Instagram)

- Recommending tools you actually use (e.g., Wise, Hostinger, Notion)

Best platforms to join:

- Amazon Associates (easy start)

- Impact.com (wide selection)

- ShareASale (digital tools)

- Wise Affiliate (global finance)

Passive income comes from the long tail: posts you wrote months ago still generating clicks.

5. Stream 3: High-Yield Savings and Cash-Back Loops

This is where your money works for you—literally.

- Open a high-yield USD savings account (e.g., 4.5–5.5% APY)

- Use cashback apps for daily spending (Rakuten, Dosh, Curve)

- Stack rewards with cashback cards + crypto cashback cards

The key? Automation. Set it up once and let the interest or cashback build silently.

6. Stream 4: Monetized Blogging (Realistic Strategy)

Blogging is not dead, it’s just evolved.

A 2025 strategy involves:

- Picking one topic: “How expats can save money abroad”

- Writing long, SEO-rich posts (1,500–3,000+ words)

- Monetizing with AdSense + affiliate links

- Promoting via Pinterest, Reddit, and SEO tools (RankMath, Ahrefs)

One well-optimized post can make $50–$500/month on its own.

7. Stream 5: YouTube + Audio Content with AI Tools

If you’re camera-shy, AI is your friend.

Use tools like:

- Pictory or Canva for video generation

- Suno or ElevenLabs for voice and music

- CapCut or Descript for editing

You can now create YouTube videos, Spotify podcasts, and shorts without filming yourself—and monetize through ads, sponsors, and affiliate links.

8. Stream 6: Print-on-Demand & Licensing

You don’t need inventory to sell products. With services like:

- Printful (T-shirts, mugs, bags)

- Redbubble or Teepublic (design platforms)

- Creative Market (sell fonts, logos, UI kits)

Upload once, earn forever. Some artists make thousands per month from one viral sticker or T-shirt.

9. Stream 7: Long-Term Investment Income

For those with capital, these are the most hands-off streams:

- Dividend-paying ETFs (e.g., VYM, SCHD)

- Real estate funds or REITs

- Crowdfunding platforms (Fundrise, RealtyMogul)

- Crypto staking (only with reputable platforms)

This strategy requires initial capital, but the returns can be fully passive and scalable.

10. How to Combine These into a Profitable Ecosystem

You don’t need to master all 7. Pick 2 or 3 and make them interconnected.

Example:

- Your blog drives traffic to your eBook

- Your eBook recommends affiliate tools

- Your affiliate links appear in your YouTube video description

Each piece supports the others. This is how top creators automate their income.

11. Final Checklist to Get Started Today

Pick 2 streams from the list

Create your first digital product or blog post

Sign up for 2 affiliate programs

Open a high-yield savings account

Schedule 1 hour per day for 30 days to build your system

12. Conclusion: Focus, Consistency, and 12-Month Goals

This isn’t a one-week sprint.

Building true passive income takes focus, content, and consistency. But if you treat it like a real business, even one year from now your system could be earning while you sleep.