Wealthy families and high-performing operators do not “collect entities.” They design architecture: a deliberate separation of ownership, control, risk, and cashflow that holds up under pressure. The aim is not secrecy; it is lawful resilience—so a lawsuit, market shock, banking hiccup, counterparty default, or political surprise in one corner does not contaminate everything else.

This article gives you a structure-first playbook you can actually run: three maps to draw, blocks to combine (trusts, foundations, holding stacks, SPVs), cash routes to document, banking rails to test, governance cadences to calendar, and stress drills to perform. No clause drafting here—only architecture, governance, and money movement engineered for durability and scale.

Main Body

1) The One-Page System: Three Maps That Keep You Honest

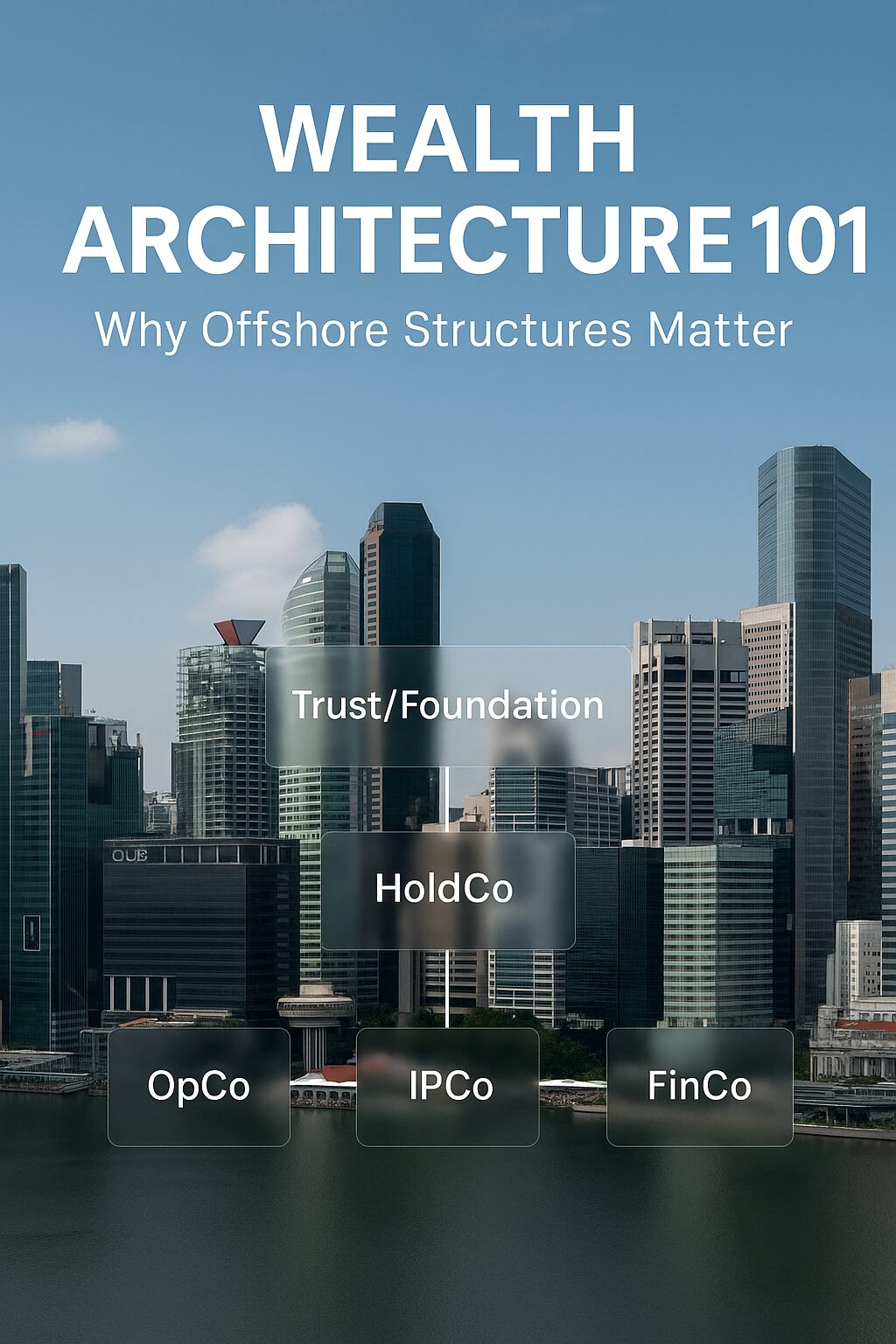

Entity Map (who owns what):

Individual → Trust or Foundation → HoldCo → {OpCo, IPCo, FinCo} → SPVs

- OpCo = revenue + employees + operational liability

- IPCo = patents/brands/code; licenses to OpCo

- FinCo = cash, custody, credit lines, hedging

- SPVs = one asset/project/JV per box; easy exits and clean quarantines

Governance Map (who can decide what):

Appoint/remove powers, voting thresholds, vetoes, conflict policies, audit cadence, and who signs what. The art is control without control—oversight that guides outcomes without day-to-day command.

Cashflow Map (what contract moves which dollars):

Dividends (OpCo→HoldCo), royalties (OpCo→IPCo), services/management fees (OpCo↔HoldCo/FinCo), wages/board fees (to humans). Each arrow needs commercial rationale, arm’s-length pricing, invoices, approvals, and a rail.

Operator ritual: Print the three maps; review quarterly. If reality drifts from the paper, fix reality or fix the paper—and minute the decision.

2) The Blocks: What Each Box Actually Does

Trusts — separate ownership from control

A trustee holds legal title for beneficiaries. A protector may oversee the trustee but must not micromanage. A letter of wishes guides intent without converting oversight into command. Trusts shine for protection and succession when reserved powers are restrained.

Private foundations — civil-law cousin with corporate bones

A legal person run by a council/board under a constitution/bylaws. Excellent where corporate-style governance, continuity, and transparent reporting are preferred.

Holding & SPV stack — the fence, not just a chart

- HoldCo owns valuable things, performs little that creates outside liability.

- OpCo touches customers and staff; keep capital light.

- IPCo holds the moat and licenses it on purpose.

- FinCo runs treasury, custody, credit, and FX policy.

- SPVs isolate assets, deals, JVs, and properties so exits are clean and contagion is rare.

Each added box must reduce real risk, improve cash movement, or upgrade governance. Ornament is cost without protection.

3) Ring-Fence Mechanics: How Risk Stays Where It Belongs

Functional segregation

- Operations risk lives in OpCo.

- Intangible value lives in IPCo and is priced by license.

- Financial firepower lives in FinCo and is never pledged casually.

- Project risk lives in SPVs—one box, one risk perimeter.

Intercompany discipline

- IP license: scope, territory, exclusivity, pricing method.

- Services: who provides what, to whom, at what basis.

- Dividend policy: solvency tests, timing windows, board approvals.

- Cost-sharing: allocation method and support memos.

- Invoices on schedule, payments on rails, reconciliations in the DMS.

Ring-Fence KPIs

- Contagion score: If OpCo implodes, can creditors reach IPCo or FinCo?

- Paper trail health: Contracts, approvals, invoices, payments, and minutes line up.

- Currency match: Inflows and outflows matched by bucket; conversions are scheduled, not reactive.

- Jurisdiction diversification: No single legal or banking point of failure.

4) Banking & Multi-Currency: The Plumbing That Makes It Real

Currency buckets

Maintain core buckets (e.g., USD/EUR/GBP plus one Asian anchor). Park revenues in the currency earned, then convert on a treasury calendar for planned uses. Publish to yourself a house spread cap; batch or reroute if quotes exceed it.

Rails

- Bank-to-bank: SWIFT / SEPA / ACH / Faster Payments.

- Revenue capture: PSP / payment gateway, settled to the right bucket.

- Custody: marketable assets held in segregated custody under the correct legal owner.

- Mandates: dual control, beneficiary whitelists, role-based limits.

Treasury SOP (short and followed)

- Two-person release for wires.

- Daily limit tiers by role.

- New beneficiary waiting period unless whitelisted.

- Weekly reconciliation; monthly spread review; quarterly fee audit.

Why this matters: Architecture without plumbing is theatre. Most failures start with one rail, one bank, one currency, and no SOP.

5) Substance: People, Premises, Processes (The Reality Check)

People

Who actually makes decisions? Evidence via employment or management agreements, director appointment letters, and time logs.

Premises

Registered offices, leases, or serviced arrangements that match the entity’s role. Use what is proportionate, but document it.

Processes

Calendared meetings with agendas, packs, minutes, resolutions, and action logs—kept in a structured DMS. Intercompany invoicing and payments run on a schedule, not at year-end panic.

Registers & filings

UBO and directors registers, annual returns, audits where applicable. Entities struck off to “save fees” is the costliest false economy.

6) Control Without Control: The Fine Line That Actually Protects You

Protection collapses when a principal retains de facto command. Courts and authorities look past the deed to how things run.

Do

- Use licensed trustees or a properly staffed foundation council.

- Calibrate protector powers to oversight (replace a failing trustee, approve distribution classes) rather than day-to-day steering.

- Keep decisions at the right organ—board/council resolutions, not personal emails.

- Maintain and periodically refresh a letter of wishes.

Don’t

- Reserve blanket vetoes over everything.

- Backdate minutes or patch invoices.

- Co-mingle funds or treat entities as interchangeable accounts.

7) Cashflow Engineering: Routes, Pricing, Evidence

Routes

- Dividends climb up from OpCo to HoldCo.

- Royalties flow from OpCo to IPCo for brand/tech use.

- Service/management fees compensate shared platforms.

- Wages/board fees pay humans for real work.

Pricing

Define a defensible method (comparable rates, cost-plus, royalty base) and keep the memo. You don’t need to publish pricing secrets—just be able to explain and evidence them.

Evidence

Board approvals, contracts, invoices, payments, bank statements, reconciliations. Missing one link weakens the chain.

8) The 30-60-90 Execution Runbook

Days 1–30 — Map & Policy

- Inventory assets, income streams, liabilities, counterparties, and key risks.

- Draft your three maps (entity/governance/cashflow).

- Approve a treasury SOP, signatory matrix, and spread caps.

- Prepare intercompany skeletons (IP license, services, cost-sharing, dividend policy).

- Choose trust vs foundation axis; shortlist fiduciaries.

Days 31–60 — Build & Bank

- Form or validate HoldCo, IPCo, FinCo; create SPVs for discrete deals/assets.

- Seat trustee or foundation council; finalize letter of wishes or bylaws.

- Open multi-currency accounts and custody; wire test amounts along each intended route.

- Calendar governance: quarterly board/council; monthly treasury review; annual audit prep.

Days 61–90 — Substance & Stress

- Seat decision-makers with contracts.

- Start live intercompany invoicing and scheduled royalties/dividends.

- Run tabletop drills: OpCo lawsuit; bank account review/freeze; gateway reserve spike; FX shock.

- Close documentation gaps; harden your document room and backups.

9) Portfolio-Aware Patterns (Pick the Stack That Fits)

Operating-business heavy

- Keep OpCo lean; push moat to IPCo; treasury in FinCo.

- Use SPVs for new product lines with uncertain liability.

- KPI: customer concentration risk and warranty tail matched with liquidity buffers.

IP-first creator or software owner

- IPCo is crown-jewel; licensing terms and audit rights crisply defined.

- OpCo pays royalties; FinCo retains runway and hedges FX on receivables.

- KPI: royalty coverage ratio and license enforcement cycle time.

Real-asset investor

- One property/deal per SPV; HoldCo manages capital allocation; FinCo manages covenants and interest rate hedges.

- KPI: debt service coverage by SPV and cross-default exposure map.

Financial portfolio & family office

- FinCo as hub with segregated custody accounts mapped to legal owners.

- Clear IPS (investment policy statement) and authority matrix.

- KPI: custody reconciliation breaks and counterparty concentration.

10) Measurement: The Five-Signal Dashboard

- Ring-Fence Score — IP and treasury insulated from OpCo failures.

- Governance Rhythm — Meetings/minutes/resolutions on cadence.

- Cashflow Discipline — Contracts issued, invoices paid, reconciled.

- Currency Hygiene — Natural hedges, scheduled conversions, spread caps enforced.

- Jurisdiction Mix — Diversification with rationale and tested rails.

Green on all five is resilient. Amber requires fixes with minutes. Red means your “architecture” is a drawing, not a system.

11) Document Room: How to Prove Reality Fast

Top-level folders

- Corporate (deeds, bylaws, registers, appointments)

- Governance (agendas, packs, minutes, resolutions)

- Intercompany (licenses, services, cost-share, memos)

- Treasury (mandates, SOP, reconciliations, spread logs)

- Custody & Banking (statements, confirmations, fee schedules)

- Compliance (UBO filings, annual returns, audits)

- Risk & Drills (stress-test notes, lessons learned)

Every file named YYYY-MM-DD_Item_Version is overkill; every audit smiles at it.

12) Common Failure Modes (and Targeted Fixes)

- Protector overreach → sham risk

Fix: Narrow powers to oversight; rewrite deed/bylaws; minute the change. - Paperless royalties/services

Fix: Issue contracts and invoices; implement monthly close with checklists. - Single-bank single-currency

Fix: Secondary rails, currency buckets, and PSP redundancy. - Empty-shell substance

Fix: Seat decision-makers, premises commensurate with function, process calendar. - Year-end clean-up culture

Fix: Move to monthly cadence; quarter-end true-ups only.

Conclusion

A resilient wealth architecture is simple to explain, hard to break, and easy to audit. It is built from a few purposeful boxes, documented routes for money, real people doing real work, rails that have been tested, and a governance rhythm that turns drawings into reality. Execute the runbook, measure the five signals, and keep your one-page system current. That is how protection, succession, and scalability stop being slogans and become the way your wealth actually operates.

Optional tool for execution: Download the ready-to-edit tracker to assign owners, dates, and links to proofs:

Asset Structure Checklist (Excel) — Download

Case Studies (placed immediately above the preview)

Success — IP Survives, Brand Lives

- Design: IPCo holds brand/code; OpCo licenses; FinCo manages cash; quarterly board cadence.

- Shock: Product liability claim hits OpCo.

- Outcome: Plaintiffs cannot reach IPCo; settlement within coverage; business continuity intact.

- Lesson: License + minutes + treasury segregation stop contagion.

Success — FX & Rail Redundancy Pays Off

- Design: Multi-currency buckets; PSP settles to matched currencies; dual-bank rails; spread caps logged.

- Shock: Primary bank imposes sudden compliance review.

- Outcome: Payments rerouted; payroll met; customers unaffected.

- Lesson: Redundancy is cheaper than rescue.

Success — Clean JV Exit via SPV

- Design: Each JV in its own SPV with shareholders’ agreement and deadlock rules.

- Shock: Strategy split with partner.

- Outcome: Sale of SPV equity; HoldCo and other assets untouched.

- Lesson: One project, one box, one exit.

Failure — “Form-Only” Trust

- Design: Settlor reserved sweeping vetoes; protector micro-managed distributions.

- Shock: Creditor challenge.

- Outcome: De facto control found; protection collapsed.

- Lesson: Oversight beats command.

Failure — Paper Trail Missing

- Design: Chart looked great; no invoices, no approvals.

- Shock: Tax inquiry.

- Outcome: Adjustments, penalties, and forced unwinds.

- Lesson: Evidence is the structure.

Failure — Single-Jurisdiction Everything

- Design: Entities, banks, and revenue in one jurisdiction.

- Shock: Local disruption and account restrictions.

- Outcome: Operations stalled; emergency restructuring under stress.

- Lesson: Diversify law, currency, and rails.

Next Article Preview

Trusts Deep Dive — Roles, Layering, and the Line You Must Not Cross

In the next part, you’ll learn how to use a discretionary trust to separate ownership from influence without inviting re-characterization. We will map the layering path (Individual → Trust → SPV), show protector powers that preserve oversight without control, and give you a fast diagnostic to spot deed provisions that quietly turn protection into illusion—so your trust works when it is most needed.