Note: This article is for informational purposes only and does not constitute financial or legal advice. Consult professionals for your specific circumstances.

Why Stablecoins Are Replacing Banks for Global Payments

Imagine sending money across the world in minutes, with almost zero fees, no bank delays, and no border restrictions.

That’s exactly what stablecoins are making possible.

While traditional banks are slow, expensive, and limited by geography, stablecoins like USDT and USDC have emerged as a borderless alternative for freelancers, remote teams, global businesses, families, and even refugees.

In this guide, we’ll show you how to use stablecoins for international payments safely, cheaply, and legally — whether you’re a digital nomad, online business owner, or just sending money to loved ones abroad.

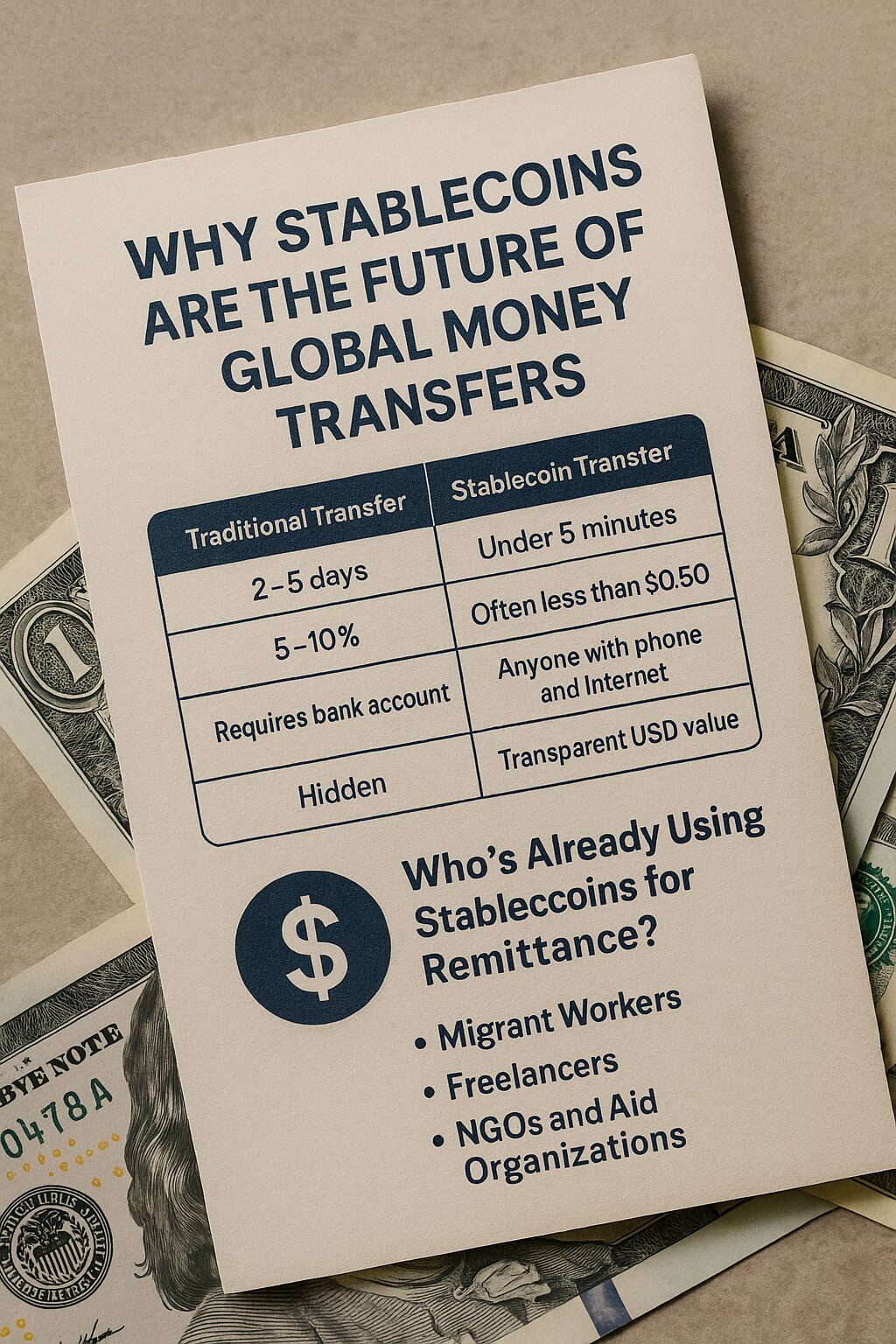

1. The Problem with Traditional Cross-Border Payments

Sending money across borders has always been a nightmare:

- Bank wires can take 3–7 business days

- Transfer fees range from $20–$100

- Currency conversion charges silently take 2–5% of the amount

- Blocked or reversed transactions due to sanctions or unclear documentation

And for people in restricted countries or unbanked regions? Access is often impossible.

2. Why Stablecoins Are a Better Global Payment Tool

Stablecoins offer a powerful solution:

- Near-instant settlement (minutes, not days)

- Transaction fees as low as $0.10

- No middlemen (no SWIFT, no intermediaries)

- Borderless — usable from Argentina to Indonesia

- Open 24/7, 365 days a year

Popular stablecoins for payments include:

- USDT (Tether) — most widely accepted

- USDC (Circle) — more regulated, preferred by businesses

- DAI (MakerDAO) — decentralized, good for censorship-resistant use

3. Real-World Use Cases

Freelancers and Contractors

- Global clients pay workers in crypto, avoiding PayPal or wire delays

- Example: Designer in India receives $1,000 USDT from U.S. client — arrives in minutes, no fees

Remote Teams and International Payroll

- Startups with global teams use USDC to pay salaries to wallets or crypto cards

- Automates global HR without banking headaches

Migrants and Families

- Families in Latin America use stablecoins to receive remittances from relatives abroad

- Cheaper and faster than Western Union

Sanctioned or Bank-Limited Areas

- People in Venezuela, Lebanon, or Myanmar use stablecoins to access global trade and income

4. How to Actually Use Stablecoins for Payments

Step 1: Choose the Right Stablecoin

- USDT for general use

- USDC for business/payroll

- DAI for privacy or DeFi use

Step 2: Set Up a Wallet

- Mobile: Trust Wallet, Rabby, Coinbase Wallet

- Browser: MetaMask

- Hardware: Ledger, Trezor

Always back up seed phrases offline!

Step 3: Get Stablecoins

- Buy on exchanges (Binance, OKX, Coinbase)

- Receive from another user

- Use crypto on-ramp (e.g., MoonPay, Transak)

Step 4: Send or Receive

- Input wallet address (double-check!)

- Send desired amount (can be as low as $1)

- Done in seconds with confirmation on-chain

5. How to Convert Stablecoins to Cash (if needed)

- Use centralized exchanges (Binance P2P, Kraken, Coinbase)

- Use local crypto OTC dealers

- Use crypto debit cards (Wirex, BitPay, Crypto.com)

- Spend directly on platforms that accept USDT/USDC

Always check local regulations before converting.

6. Legal and Regulatory Considerations

Stablecoin payments are legal in most countries — but documentation and tax reporting may apply.

Things to consider:

- Declare income if used for business/freelance

- Store transaction history (tools: Koinly, CoinTracking)

- Comply with capital control rules in restricted countries

- Avoid mixing with high-risk wallets or mixers

In most cases, using stablecoins for sending/receiving is safer than holding long-term, legally speaking.

7. How to Keep Transactions Safe and Private

- Always verify wallet addresses before sending

- Use encrypted messaging for addresses (not public chats)

- Avoid sharing wallet screenshots or public explorer links

- Use privacy wallets if needed (e.g., Rabby or Wasabi for BTC-based stablecoins)

- Be cautious with QR codes — confirm destination manually

Conclusion: Stablecoins Are the New Global Wire Transfer

Stablecoins have turned smartphones into international money hubs — accessible to anyone, anywhere, anytime.

No matter your use case — remote income, family support, or payroll — they offer:

- Speed

- Low cost

- Flexibility

- Borderless freedom

But to unlock these benefits safely:

- Learn the tools

- Document the flows

- Respect legal frameworks

Done right, stablecoins don’t just move money — they move opportunity.