Introduction: Why Budgeting Is Broken in 2025

The world has changed. With inflation spikes, currency instability, and the rise of freelance and remote work, traditional budgeting no longer works. You might have tried the 50/30/20 rule or envelope system. But if you’ve moved between countries, earn in multiple currencies, or juggle fluctuating income, you’ve probably discovered these methods fail in real-world chaos.

The Global Budgeting System is the first budgeting framework designed for today’s global reality—one that gives you flexibility, control, and clarity no matter where you are or how much you earn.

Part 1: What Makes Global Budgeting Different?

Most budgeting methods assume:

- Fixed income

- Stable currency

- Static living location

But if you’re like millions today, you might:

- Earn in dollars but spend in pesos, euros, or baht

- Freelance with unpredictable income

- Move countries frequently (or live a “nomadic” lifestyle)

- Need to manage expenses across bank accounts in multiple countries

Global Budgeting is:

- Currency-Agnostic: Budget in a base currency of your choice (USD, EUR, etc.), while tracking spending in local currencies.

- Income-Responsive: Dynamically adjusts based on monthly income fluctuation.

- Portable: Fully cloud-based and bank-independent.

- Tax-Optimized: Helps you allocate for taxes regardless of where you earn.

Part 2: The Core Structure of the Global Budgeting System

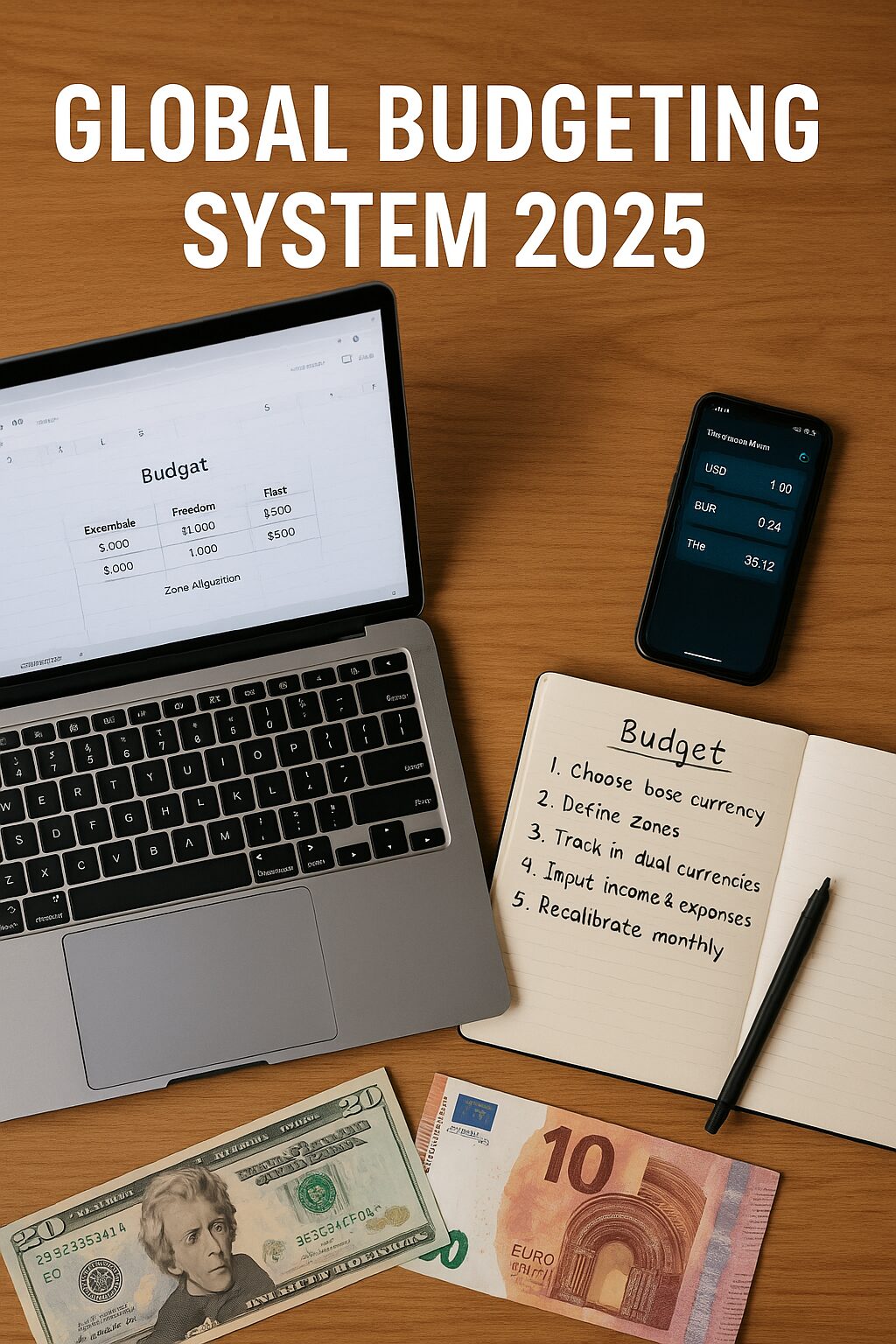

1. Three-Zone Allocation

This replaces outdated percentages with zones:

- Essentials Zone (EZ) – Everything you must pay to survive and function (rent, food, transport, health).

- Freedom Zone (FZ) – The money that gives you future options (savings, investments, debt repayment).

- Flex Zone (FX) – Lifestyle spending (restaurants, travel, hobbies).

Rather than rigid ratios, each zone expands/contracts with income shifts.

2. Dual-Currency Tracking

You track expenses in:

- Your chosen base currency (USD recommended)

- Local currency using real-time exchange rates via automated spreadsheets or apps (e.g., Notion, Tiller, Excel w/ PowerQuery)

This removes currency-blindness—one of the biggest silent budget killers for global earners.

3. Monthly Recalibration Ritual

At the end of each month, perform:

- Zone Audit: Did EZ, FZ, and FX match your intentions?

- Currency Drift Check: How much did exchange rates affect you?

- Adjustment Session: Reallocate based on next month’s realities.

Part 3: How to Set It Up (Step-by-Step)

Step 1: Choose a Base Currency

Pick the currency you think in—usually USD for global use. All zones will be defined in this currency.

Step 2: Define Your Zones

Based on last 3 months, decide your average split across EZ, FZ, and FX. For example:

- EZ: $1,500

- FZ: $1,000

- FX: $500

Step 3: Create a Dual-Currency Tracker

You can use:

- A Google Sheet with exchange rate API connection

- Notion finance dashboard

- Tiller or YNAB (with multi-currency plugins)

Step 4: Input All Income and Expenses

- Income in whatever currency you earn

- Spending in the local currency of the country you’re in

- Tracker automatically converts to base currency

Step 5: Recalibrate Monthly

Look at drift and over/under-spending by zone. Adjust zone caps if income changed significantly.

Part 4: Real-World Example – Remote Worker in Thailand

Base Currency: USD

Income: $3,000/month from Upwork

Spending Currency: Thai Baht (THB)

- EZ (Essentials): Rent, groceries, SIM card, transportation = ~25,000 THB → $700

- FZ (Freedom): Roth IRA, crypto, U.S. taxes, student loans = $1,200

- FX (Flex): Cafes, coworking, travel = ~15,000 THB → $400

- Buffer = $700 for unexpected expenses

With the Global Budgeting Sheet, he sees his USD position in real time, sets his Thai Baht ATM withdrawals based on pre-converted targets, and avoids overspending despite income fluctuation.

Part 5: Benefits Over Traditional Budgeting

| Traditional Budgeting | Global Budgeting |

|---|---|

| Fixed ratios | Dynamic, zone-based |

| Local-only currency | Multi-currency |

| One-country use | Global mobility |

| Manual tracking | Automated tools |

| No tax planning | Tax-aware allocation |

This system empowers freelancers, digital nomads, remote workers, and even retirees living abroad to gain true control over their money.

Part 6: Tools to Use (2025 Edition)

- Tiller Money + Google Sheets (with currency plugin)

- Notion Finance Tracker Templates (search “multi-currency budgeting”)

- Excel + PowerQuery for advanced automation

- Revolut / Wise for multi-currency banking

Optional: Use ChatGPT + Google Sheets for monthly zone reports.

Part 7: Final Thoughts

In 2025, financial freedom means global flexibility. If your budgeting system can’t keep up with your income streams, travel life, or multi-currency reality, you’re at risk of invisible leaks and financial drift.

The Global Budgeting System is how real people manage real money in the real world now.

This isn’t theory—it’s practice for anyone ready to build a flexible, international life with total control over their money.

Introduction: Why Budgeting Is Broken in 2025

The world has changed. With inflation spikes, currency instability, and the rise of freelance and remote work, traditional budgeting no longer works. You might have tried the 50/30/20 rule or envelope system. But if you’ve moved between countries, earn in multiple currencies, or juggle fluctuating income, you’ve probably discovered these methods fail in real-world chaos.

The Global Budgeting System is the first budgeting framework designed for today’s global reality—one that gives you flexibility, control, and clarity no matter where you are or how much you earn.

Part 1: What Makes Global Budgeting Different?

Most budgeting methods assume:

- Fixed income

- Stable currency

- Static living location

But if you’re like millions today, you might:

- Earn in dollars but spend in pesos, euros, or baht

- Freelance with unpredictable income

- Move countries frequently (or live a “nomadic” lifestyle)

- Need to manage expenses across bank accounts in multiple countries

Global Budgeting is:

- Currency-Agnostic: Budget in a base currency of your choice (USD, EUR, etc.), while tracking spending in local currencies.

- Income-Responsive: Dynamically adjusts based on monthly income fluctuation.

- Portable: Fully cloud-based and bank-independent.

- Tax-Optimized: Helps you allocate for taxes regardless of where you earn.

Part 2: The Core Structure of the Global Budgeting System

1. Three-Zone Allocation

This replaces outdated percentages with zones:

- Essentials Zone (EZ) – Everything you must pay to survive and function (rent, food, transport, health).

- Freedom Zone (FZ) – The money that gives you future options (savings, investments, debt repayment).

- Flex Zone (FX) – Lifestyle spending (restaurants, travel, hobbies).

Rather than rigid ratios, each zone expands/contracts with income shifts.

2. Dual-Currency Tracking

You track expenses in:

- Your chosen base currency (USD recommended)

- Local currency using real-time exchange rates via automated spreadsheets or apps (e.g., Notion, Tiller, Excel w/ PowerQuery)

This removes currency-blindness—one of the biggest silent budget killers for global earners.

3. Monthly Recalibration Ritual

At the end of each month, perform:

- Zone Audit: Did EZ, FZ, and FX match your intentions?

- Currency Drift Check: How much did exchange rates affect you?

- Adjustment Session: Reallocate based on next month’s realities.

Part 3: How to Set It Up (Step-by-Step)

Step 1: Choose a Base Currency

Pick the currency you think in—usually USD for global use. All zones will be defined in this currency.

Step 2: Define Your Zones

Based on last 3 months, decide your average split across EZ, FZ, and FX. For example:

- EZ: $1,500

- FZ: $1,000

- FX: $500

Step 3: Create a Dual-Currency Tracker

You can use:

- A Google Sheet with exchange rate API connection

- Notion finance dashboard

- Tiller or YNAB (with multi-currency plugins)

Step 4: Input All Income and Expenses

- Income in whatever currency you earn

- Spending in the local currency of the country you’re in

- Tracker automatically converts to base currency

Step 5: Recalibrate Monthly

Look at drift and over/under-spending by zone. Adjust zone caps if income changed significantly.

Part 4: Real-World Example – Remote Worker in Thailand

Base Currency: USD

Income: $3,000/month from Upwork

Spending Currency: Thai Baht (THB)

- EZ (Essentials): Rent, groceries, SIM card, transportation = ~25,000 THB → $700

- FZ (Freedom): Roth IRA, crypto, U.S. taxes, student loans = $1,200

- FX (Flex): Cafes, coworking, travel = ~15,000 THB → $400

- Buffer = $700 for unexpected expenses

With the Global Budgeting Sheet, he sees his USD position in real time, sets his Thai Baht ATM withdrawals based on pre-converted targets, and avoids overspending despite income fluctuation.

Part 5: Benefits Over Traditional Budgeting

| Traditional Budgeting | Global Budgeting |

|---|---|

| Fixed ratios | Dynamic, zone-based |

| Local-only currency | Multi-currency |

| One-country use | Global mobility |

| Manual tracking | Automated tools |

| No tax planning | Tax-aware allocation |

This system empowers freelancers, digital nomads, remote workers, and even retirees living abroad to gain true control over their money.

Part 6: Tools to Use (2025 Edition)

- Tiller Money + Google Sheets (with currency plugin)

- Notion Finance Tracker Templates (search “multi-currency budgeting”)

- Excel + PowerQuery for advanced automation

- Revolut / Wise for multi-currency banking

Optional: Use ChatGPT + Google Sheets for monthly zone reports.

Part 7: Final Thoughts

In 2025, financial freedom means global flexibility. If your budgeting system can’t keep up with your income streams, travel life, or multi-currency reality, you’re at risk of invisible leaks and financial drift.

The Global Budgeting System is how real people manage real money in the real world now.

This isn’t theory—it’s practice for anyone ready to build a flexible, international life with total control over their money.

Introduction: Why Budgeting Is Broken in 2025

The world has changed. With inflation spikes, currency instability, and the rise of freelance and remote work, traditional budgeting no longer works. You might have tried the 50/30/20 rule or envelope system. But if you’ve moved between countries, earn in multiple currencies, or juggle fluctuating income, you’ve probably discovered these methods fail in real-world chaos.

The Global Budgeting System is the first budgeting framework designed for today’s global reality—one that gives you flexibility, control, and clarity no matter where you are or how much you earn.

Part 1: What Makes Global Budgeting Different?

Most budgeting methods assume:

- Fixed income

- Stable currency

- Static living location

But if you’re like millions today, you might:

- Earn in dollars but spend in pesos, euros, or baht

- Freelance with unpredictable income

- Move countries frequently (or live a “nomadic” lifestyle)

- Need to manage expenses across bank accounts in multiple countries

Global Budgeting is:

- Currency-Agnostic: Budget in a base currency of your choice (USD, EUR, etc.), while tracking spending in local currencies.

- Income-Responsive: Dynamically adjusts based on monthly income fluctuation.

- Portable: Fully cloud-based and bank-independent.

- Tax-Optimized: Helps you allocate for taxes regardless of where you earn.

Part 2: The Core Structure of the Global Budgeting System

1. Three-Zone Allocation

This replaces outdated percentages with zones:

- Essentials Zone (EZ) – Everything you must pay to survive and function (rent, food, transport, health).

- Freedom Zone (FZ) – The money that gives you future options (savings, investments, debt repayment).

- Flex Zone (FX) – Lifestyle spending (restaurants, travel, hobbies).

Rather than rigid ratios, each zone expands/contracts with income shifts.

2. Dual-Currency Tracking

You track expenses in:

- Your chosen base currency (USD recommended)

- Local currency using real-time exchange rates via automated spreadsheets or apps (e.g., Notion, Tiller, Excel w/ PowerQuery)

This removes currency-blindness—one of the biggest silent budget killers for global earners.

3. Monthly Recalibration Ritual

At the end of each month, perform:

- Zone Audit: Did EZ, FZ, and FX match your intentions?

- Currency Drift Check: How much did exchange rates affect you?

- Adjustment Session: Reallocate based on next month’s realities.

Part 3: How to Set It Up (Step-by-Step)

Step 1: Choose a Base Currency

Pick the currency you think in—usually USD for global use. All zones will be defined in this currency.

Step 2: Define Your Zones

Based on last 3 months, decide your average split across EZ, FZ, and FX. For example:

- EZ: $1,500

- FZ: $1,000

- FX: $500

Step 3: Create a Dual-Currency Tracker

You can use:

- A Google Sheet with exchange rate API connection

- Notion finance dashboard

- Tiller or YNAB (with multi-currency plugins)

Step 4: Input All Income and Expenses

- Income in whatever currency you earn

- Spending in the local currency of the country you’re in

- Tracker automatically converts to base currency

Step 5: Recalibrate Monthly

Look at drift and over/under-spending by zone. Adjust zone caps if income changed significantly.

Part 4: Real-World Example – Remote Worker in Thailand

Base Currency: USD

Income: $3,000/month from Upwork

Spending Currency: Thai Baht (THB)

- EZ (Essentials): Rent, groceries, SIM card, transportation = ~25,000 THB → $700

- FZ (Freedom): Roth IRA, crypto, U.S. taxes, student loans = $1,200

- FX (Flex): Cafes, coworking, travel = ~15,000 THB → $400

- Buffer = $700 for unexpected expenses

With the Global Budgeting Sheet, he sees his USD position in real time, sets his Thai Baht ATM withdrawals based on pre-converted targets, and avoids overspending despite income fluctuation.

Part 5: Benefits Over Traditional Budgeting

| Traditional Budgeting | Global Budgeting |

|---|---|

| Fixed ratios | Dynamic, zone-based |

| Local-only currency | Multi-currency |

| One-country use | Global mobility |

| Manual tracking | Automated tools |

| No tax planning | Tax-aware allocation |

This system empowers freelancers, digital nomads, remote workers, and even retirees living abroad to gain true control over their money.

Part 6: Tools to Use (2025 Edition)

- Tiller Money + Google Sheets (with currency plugin)

- Notion Finance Tracker Templates (search “multi-currency budgeting”)

- Excel + PowerQuery for advanced automation

- Revolut / Wise for multi-currency banking

Optional: Use ChatGPT + Google Sheets for monthly zone reports.

Part 7: Final Thoughts

In 2025, financial freedom means global flexibility. If your budgeting system can’t keep up with your income streams, travel life, or multi-currency reality, you’re at risk of invisible leaks and financial drift.

The Global Budgeting System is how real people manage real money in the real world now.

This isn’t theory—it’s practice for anyone ready to build a flexible, international life with total control over their money.

글로벌 예산 시스템: 어디서든 돈을 통제하는 실용적인 방법 (2025년판)

2025년, 전통적인 예산 시스템은 왜 망가졌는가?

물가 상승, 통화 불안, 프리랜서 및 원격 근무 확산 등으로 인해 기존의 예산 시스템은 더 이상 유효하지 않습니다. 50/30/20 법칙이나 봉투 예산법을 시도해봤지만, 수입이 변동하거나 여러 나라에서 소비하거나 여러 통화를 사용한다면 금방 벽에 부딪히게 됩니다.

**글로벌 예산 시스템(Global Budgeting System)**은 2025년의 세계적 현실에 맞춰 설계된 최초의 예산 전략입니다. 어디에 살든, 어떤 통화로 벌든, 이 시스템은 유연하면서도 강력한 통제력을 제공합니다.

1부: 기존 예산 시스템과의 차이점

기존 시스템은 다음을 전제로 합니다:

- 고정된 수입

- 안정된 통화

- 정해진 거주지

하지만 요즘 사람들은:

- 달러로 벌고 페소나 유로, 바트로 소비함

- 수입이 매달 다름 (프리랜서/비정규직)

- 해외 이주 또는 디지털 노마드 생활 중

- 여러 국가에 계좌를 보유 중

글로벌 예산 시스템은 다음이 가능합니다:

- 통화 비의존적 (원하는 기준 통화로 예산 설정)

- 수입 연동형 (수입 변동에 따라 동적으로 예산 재편)

- 휴대 가능성 (클라우드 기반, 은행 독립적)

- 세금 대응형 (국가별 세금 대응 가능)

2부: 글로벌 예산 시스템의 구조

1) 3구역 분배법 (Three-Zone Allocation)

- 생존 구역 (Essentials Zone) – 집세, 식비, 건강, 교통 등 필수 지출

- 자유 구역 (Freedom Zone) – 저축, 투자, 부채 상환, 세금 등 미래를 위한 지출

- 자유시간 구역 (Flex Zone) – 외식, 여행, 여가 소비

퍼센트가 아닌 **’구역별 금액’**을 중심으로 구성하며 수입 변동에 따라 조절됩니다.

2) 이중 통화 추적

- 기본 통화(예: USD) 기준으로 예산 수립

- 실제 소비는 현지 통화(예: THB)로 입력 → 자동 변환

3) 월간 리셋 루틴

- 구역별 소비 비교

- 환율 변동 확인

- 다음 달 계획 조정

3부: 설정 방법 (실행 가이드)

- 기준 통화 선택 (예: USD)

- 3개 구역의 월 평균 예산 설정

- 이중 통화 예산 추적기 구축 (구글시트/노션 추천)

- 수입/지출 입력 → 자동 변환

- 매월 리셋하고 구역 조정

4부: 실제 예 – 태국 거주 원격 근무자

- 기준 통화: USD

- 수입: 월 $3,000 (Upwork)

- 지출 통화: THB

지출 예:

- EZ: 25,000THB → $700

- FZ: 투자/세금/빚 → $1,200

- FX: 여가 → 15,000THB → $400

- 예비비: $700

5부: 전통 방식보다 우위인 점

| 전통 예산 | 글로벌 예산 |

|---|---|

| 고정 비율 | 유동적 구역 |

| 단일 통화 | 다중 통화 |

| 한 국가 전용 | 다국가 사용 가능 |

| 수동 관리 | 자동화 도구 |

| 세금 고려 없음 | 세금 고려 포함 |

6부: 추천 도구 (2025년판)

- Tiller + Google Sheets (환율 플러그인)

- Notion 멀티 통화 템플릿

- Excel + PowerQuery

- Wise, Revolut

- ChatGPT 자동 리포트 기능 활용 가능

7부: 결론

2025년에는 예산이 이동성과 통제를 동시에 제공해야 합니다. 그래야 다양한 수입과 소비 구조 속에서도 재정적 자유를 누릴 수 있습니다.

글로벌 예산 시스템은 단순한 이론이 아니라 실제로 적용 가능한 도구이며, 특히 전 세계를 무대로 살아가는 모든 사람들에게 새로운 재정의 기준이 될 수 있습니다.