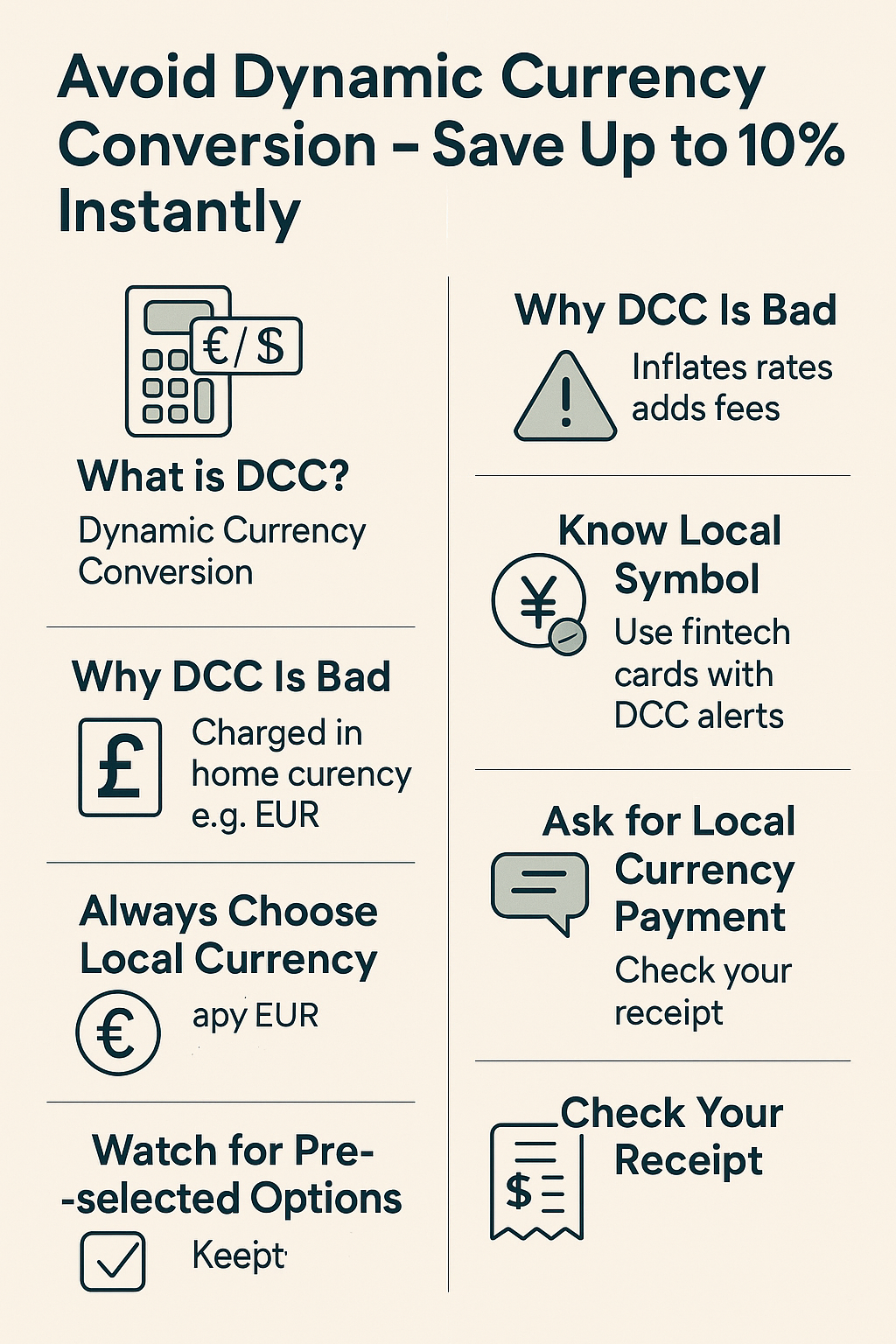

If you’re spending money abroad — whether as a digital nomad, traveler, or remote worker — foreign transaction fees can quietly drain your wallet. These charges (typically 1–3%) may seem small but can add up quickly over time.

Here are the top 5 credit cards in 2025 that do not charge foreign transaction fees, saving you real money while traveling the world.

1. Chase Sapphire Preferred® Card

Best for: Frequent travelers who want rewards and travel insurance

- No foreign transaction fees

- 2x points on travel & dining

- Built-in trip delay/cancellation/interruption coverage

- Primary rental car insurance

Annual Fee: $95

Why it’s great:

You earn points on everyday travel spending and get premium protection without the premium card fee.

2. Capital One Venture Rewards Credit Card

Best for: Simple rewards system with flexible redemptions

- No foreign transaction fees

- 2x miles on all purchases

- Redeem miles for travel, statement credit, or gift cards

- Global Entry/TSA PreCheck credit

Annual Fee: $95

Why it’s great:

Flat-rate miles means you don’t have to memorize categories — spend freely anywhere in the world.

3. Citi Premier® Card

Best for: Maximizing points on international expenses

- No foreign transaction fees

- 3x points on airfare, hotels, gas, and restaurants

- Points can be transferred to travel partners (including international airlines)

Annual Fee: $95

Why it’s great:

Earn more in the categories you actually use abroad — like flights and food.

4. Charles Schwab Debit Card (Not a credit card, but a secret weapon)

Best for: ATM cash withdrawals without fees anywhere in the world

- No foreign transaction fees

- Unlimited worldwide ATM fee reimbursements

- No monthly fees or minimum balance

- Great for cash-heavy countries

Annual Fee: $0

Why it’s great:

You’ll get ATM fees reimbursed automatically, even in remote places. An excellent backup to any travel card.

5. Wise Travel Card

Best for: Currency conversion transparency and global accessibility

- Not technically a credit card (prepaid debit), but excellent for foreign use

- No markup on currency conversion (real exchange rate)

- Supports 50+ currencies

- Instant freeze/unfreeze via app

Annual Fee: $0 (no ongoing fee)

Why it’s great:

Ideal for digital nomads who want to manage multiple currencies while avoiding banks altogether.

Final Tip: Always Notify Your Bank Before Traveling

Even if your card has no foreign transaction fees, a flagged international transaction could result in a blocked card. Use your banking app or call ahead.

Conclusion: Avoid Fees, Keep More

You don’t have to pay extra just for using your card overseas.

By choosing the right credit card — or card combination — you can save hundreds of dollars a year, without changing how you spend.

Want to be smart about your money abroad? Start by eliminating unnecessary fees.