Sending money abroad shouldn’t cost you a fortune. Yet traditional banks and remittance services can quietly deduct 2–3% (or more) from every transfer through flat fees, poor exchange rates, and middle-bank charges. Over time, those hidden costs add up, eroding hundreds of dollars from your hard-earned funds.

Below is a concise guide—under 800 words—that distills the most effective strategies to cut your international transfer costs to nearly zero.

1. Set Up Rate Alerts and Strike at the Right Moment

Exchange rates fluctuate constantly. Capturing even a 0.5% improvement on a single large transfer can save you tens of dollars.

- Choose your target rate. On platforms like Wise or Revolut, set a custom alert for the exchange rate you need (e.g., 1 USD = 0.92 EUR).

- Receive instant notifications. As soon as the market hits your rate, you’ll get an email or push notification.

- Execute immediately. Avoid manual checking: let the alert trigger your transfer so you lock in savings without delay.

Why it matters: A 0.5% gain on $5,000 is $25 saved in one transaction—compounded over time, that’s significant.

2. Use Batch Payments for Multiple Recipients

If you send to several people each month—freelancers, family members, or contractors—batch payments eliminate repeated fixed fees and manual work.

- Upload a spreadsheet. Prepare a CSV listing each recipient’s name, account details, and amount.

- One-click approval. Review the batch in your dashboard, then confirm all payments simultaneously.

- Avoid per-transfer flat fees. Rather than $5 per person, you pay a single, small percentage fee on the total.

Why it matters: Sending 10 separate $200 transfers at $5 each costs $50 in flat fees. Batch payments may reduce that to a single $3–$5 fee, saving over 90%.

3. Hold and Convert in Multiple Currencies

Rather than converting a large lump sum all at once, maintain balances in key currencies and exchange when rates are favorable.

- Open a multi-currency account. Services like Wise let you hold dozens of currencies under one login.

- Watch your “buy” thresholds. Decide the rate at which you’re comfortable converting (e.g., 1 USD = 0.89 EUR).

- Execute in pieces. Top up your EUR balance in smaller increments whenever the market dips below your threshold.

Why it matters: If you convert $10,000 in two tranches—$5,000 at 1 USD = 0.90 EUR and $5,000 at 1 USD = 0.92 EUR—you average 1 USD = 0.91 EUR, saving more than converting the full amount at a single, lower rate.

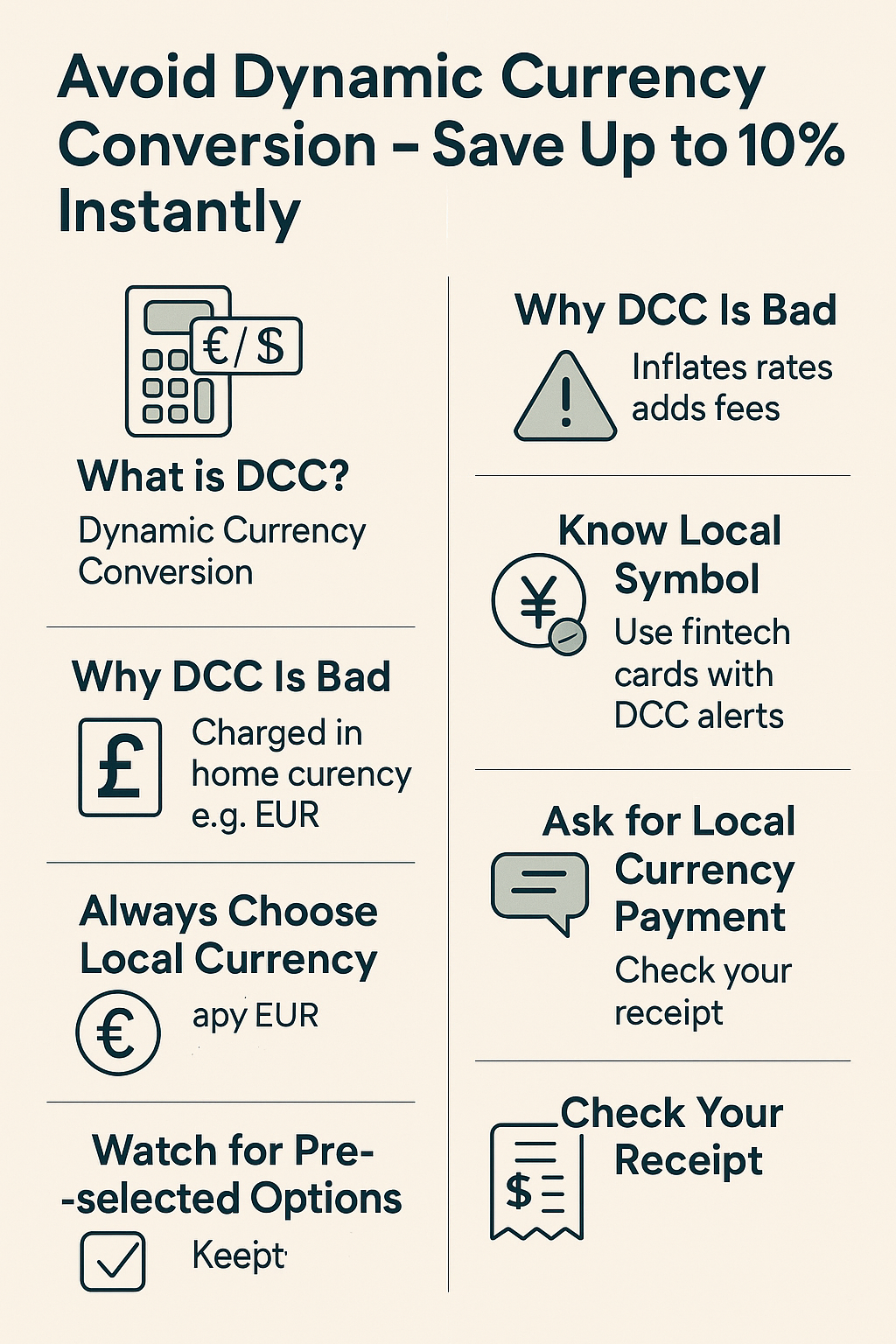

4. Spend Abroad at True Mid-Market Rates

When traveling or making online purchases in foreign currency, avoid dynamic currency conversion (DCC) and merchant markups.

- Use a fee-transparent debit card. A Wise or Revolut card charges you exactly the mid-market rate shown on Google or XE.

- Decline DCC at checkout. If a retailer prompts you to pay in your home currency, always choose to pay in the local currency.

- Link to mobile wallets. Add your card to Apple Pay or Google Pay to prevent merchants from slipping in hidden fees.

Why it matters: A 1% markup on a €1,000 hotel bill is €10 lost. Over multiple purchases, these charges quickly eclipse any annual foreign-transaction fee.

5. Automate Transfers via API for Recurring Payments

For businesses, freelancers, or anyone with regular payouts, API integration streamlines the process and slashes manual errors.

- Connect your accounting software. Platforms like Xero, QuickBooks, or Zoho Books often support direct Wise integration.

- Trigger on invoices or schedules. Automate payroll, vendor bills, or subscription refunds at set dates.

- Maintain an auditable trail. Each transaction is logged with metadata, simplifying reporting and compliance.

Why it matters: Automating a $50,000 monthly payroll at 0.4% fee costs $200. Manual wires at 1.5% (plus $30 flat) would cost $780—almost four times as much.

Putting It All Together

- Audit your past transfers. Calculate total fees paid over the last 6–12 months.

- Sign up and verify. Create accounts on Wise (or similar), complete KYC, and fund your multi-currency balances.

- Configure alerts. Set up your desired exchange-rate targets and notification channels.

- Schedule batch or recurring transfers. Migrate bulk payouts and regular payments to batch or API methods.

- Use your card wisely. Pay abroad at true rates, always refusing DCC.

By combining these five tactics—rate alerts, batch payments, multi-currency holding, transparent card spending, and API automation—you can drive your per-transfer fee below 0.3% and, in many cases, effectively to zero.

Start today, keep 100% of your money, and watch your savings grow over every international transfer.