For decades, international money transfers have been slow, expensive, and complicated. But a quiet revolution is taking place—and it’s powered by stablecoins. These dollar-pegged digital assets are rapidly reshaping how families, freelancers, and businesses send money across borders.

In this post, we’ll explore why stablecoins are disrupting the $800+ billion global remittance industry, how they eliminate the middlemen, and what this means for your wallet—whether you’re sending $50 or $5,000.

The Problem with Traditional Cross-Border Payments

Let’s face it—sending money internationally has long been a hassle.

- High Fees: Western Union, MoneyGram, and banks charge between 3% to 10%

- Slow Transfers: 2 to 5 business days is still the norm

- Hidden Costs: Poor exchange rates, wire fees, receiving charges

- Bank Dependency: Billions of people lack reliable access to financial institutions

The World Bank estimates that global remittance fees average 6.3%, with the worst rates affecting the poorest nations.

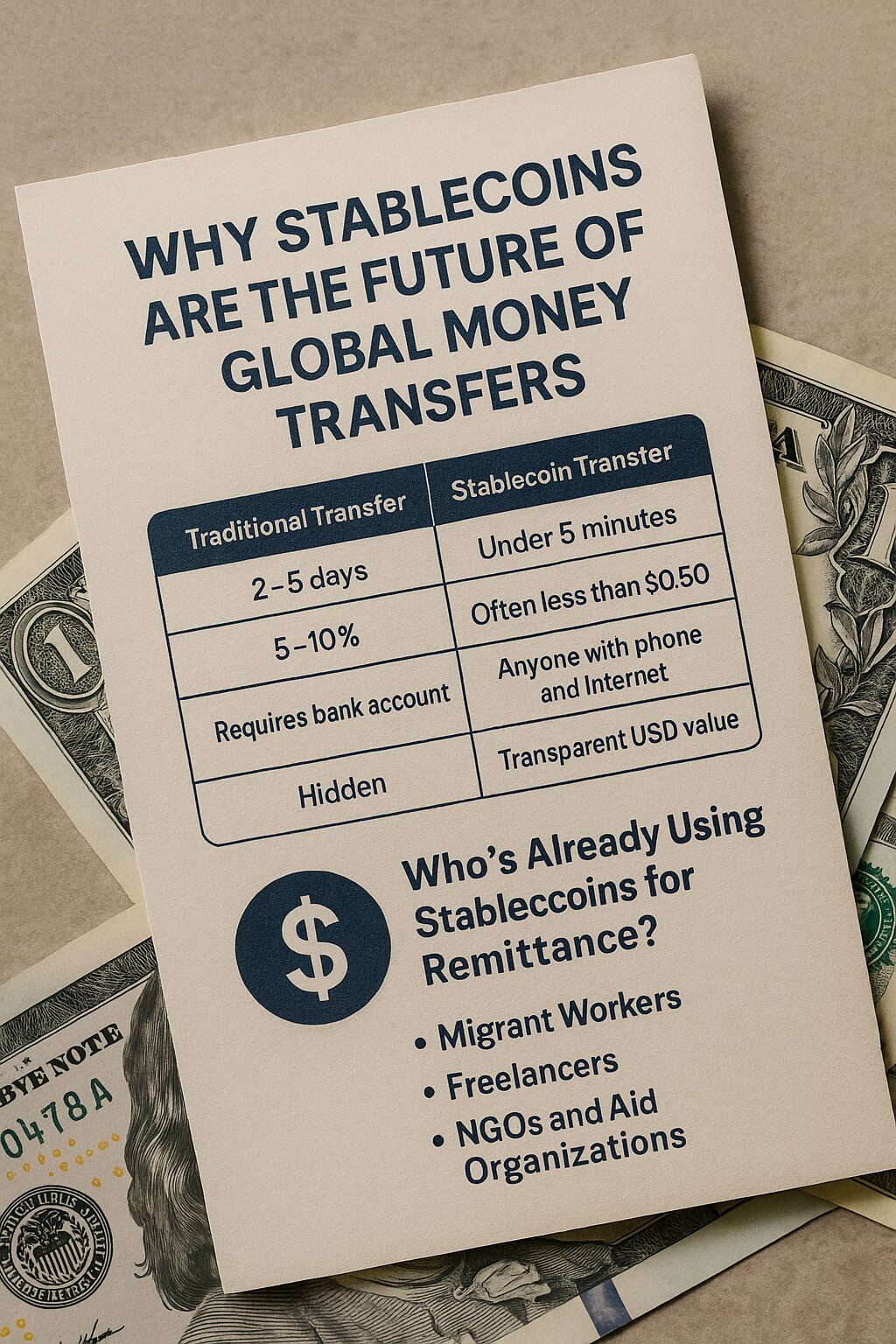

How Stablecoins Are Changing the Game

Stablecoins like USDC, USDT, DAI, and others offer a radically different experience:

| Feature | Traditional Transfer | Stablecoin Transfer |

|---|---|---|

| Speed | 2–5 days | Under 5 minutes |

| Fees | 5–10% | Often less than $0.50 |

| Access | Requires bank account | Anyone with a phone and internet |

| Currency Loss | Hidden in conversion rates | Transparent USD value |

| Availability | Office hours only | 24/7/365, even weekends |

Who’s Already Using Stablecoins for Remittance?

1. Migrant Workers

Filipino and Mexican workers are sending USDC to family members via mobile wallets, avoiding banks entirely.

2. Freelancers

Designers and developers in India and Argentina receive USDT from U.S. and EU clients—fast and free from FX losses.

3. NGOs and Aid Organizations

In regions like Venezuela and Sudan, humanitarian groups are distributing DAI to recipients who lack stable local currency.

Real-World Platforms Enabling Stablecoin Transfers

Here are some platforms that are quietly powering the stablecoin money revolution:

- Circle (USDC issuer) – Offers APIs for businesses to integrate stablecoin payouts

- Bitrefill – Lets users spend stablecoins on real-world goods and services

- Celo – Mobile-first blockchain with a focus on emerging markets

- Binance Pay – Send and receive USDT/USDC with zero fees

- Transak / Ramp / MoonPay – On-ramps from fiat to stablecoin for local accessibility

Why It Matters: The Global Inclusion Angle

Stablecoins are more than just a fintech upgrade—they’re a leap toward financial inclusion:

- 1.4 billion adults are unbanked

- Many live in countries with double-digit inflation

- Remittances are a lifeline, often over 10% of GDP in developing nations

By allowing users to send digital dollars instantly and affordably, stablecoins give control back to the people—not just banks or governments.

Are There Any Risks?

Of course. Responsible use matters. Consider these:

- Volatility of exchange rates when cashing out locally

- Dependence on platforms for wallet custody

- Regulatory changes in your country

- Scams or unverified wallet addresses

🛡️ Safety Tips:

- Only use verified platforms or exchanges

- Double-check recipient wallet addresses

- Educate family members on crypto basics before sending

- Diversify storage (cold wallets, multi-sig, etc.)

Use Cases: When Stablecoin Transfers Make the Most Sense

| Use Case | Why Stablecoins Work |

|---|---|

| Paying overseas freelancers | Instant, low-cost, no wire delays |

| Supporting family abroad | Direct, transparent value transfer |

| Settling invoices | Ideal for cross-border B2B payments |

| Travel funds backup | Mobile wallets with stable value |

| Aid distribution | Transparent tracking, programmable funds |

Final Thoughts: The Future Is Already Here

While banks and remittance giants are busy defending their old systems, millions of users are already embracing stablecoins as their primary method for moving money across borders. The benefits are simply too strong to ignore: speed, cost, access, and transparency.

For the first time in history, anyone with a smartphone can send real dollars—no banks, no paperwork, no permission required.