How banks quietly eat away your money when you go global—and how to stop them

When dealing with international banking—whether you’re moving abroad, investing overseas, working as an expat, or simply sending money back home—the hidden risks can cost you dearly. From outrageous fees to currency manipulation and blocked access, many users don’t realize they’re walking into costly traps until it’s too late.

This guide reveals the 5 most common traps in global banking, backed by real-world examples and, more importantly, how to avoid them completely.

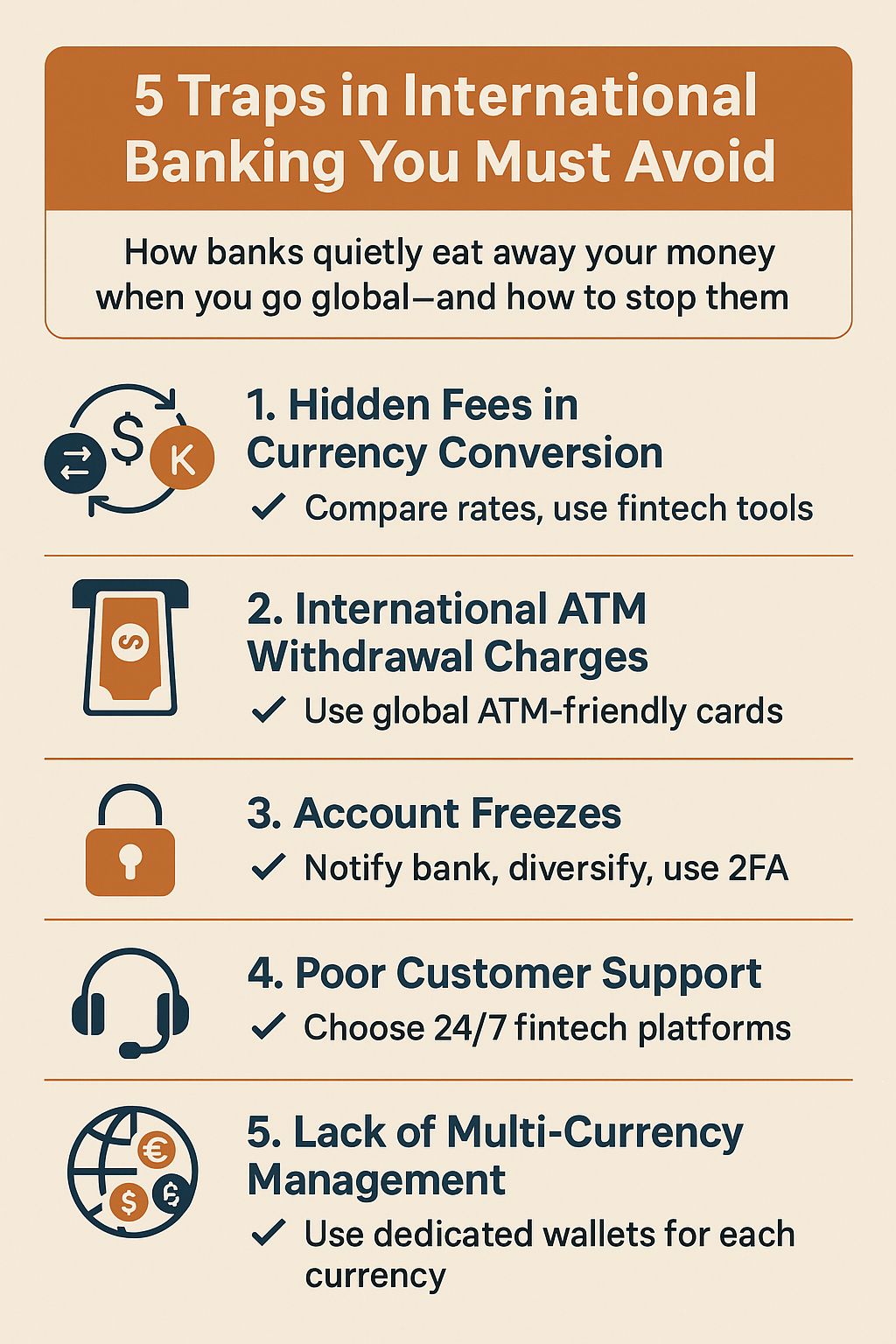

1. Hidden Fees in Currency Conversion

International banks rarely offer you the true market exchange rate. Instead, they add a spread (also called a markup) to the rate. It’s subtle but deadly.

Example: The real exchange rate is 1 USD = 1.300 KRW. Your bank gives you 1.250 KRW. That’s nearly 4% lost in conversion—and it’s often not disclosed upfront.

What You Can Do:

- Always compare exchange rates on XE.com, OANDA, or Google before using your bank.

- Switch to fintech services like Wise or Revolut for mid-market rates and fee transparency.

- Avoid changing money at airports or banks without published rates.

2. International ATM Withdrawal Charges

When you withdraw cash abroad using your home bank’s card, you’re usually hit with three types of fees:

- Your bank’s international transaction fee (often 1–3%)

- The ATM operator’s usage fee

- Currency conversion spread

Together, these can cost you $5–10 or more per withdrawal, especially on small amounts.

What You Can Do:

- Use cards from banks that refund ATM fees worldwide (e.g., Charles Schwab in the U.S.).

- Withdraw larger amounts less frequently.

- Use fintech debit cards (Wise, Revolut) that minimize foreign ATM costs.

3. Account Freezes Due to “Unusual Activity”

This is one of the most stressful traps.

If your home bank detects what they consider “suspicious” activity—such as multiple transactions from another country—they can freeze your account without warning. You could be stranded abroad with no access to your funds.

Real Case: An American expat in Thailand found her account frozen after logging in via a local IP and making hotel payments. It took 2 weeks to unlock her funds.

What You Can Do:

- Inform your bank before traveling or moving abroad.

- Enable 2FA and set up account alerts.

- Diversify your accounts across at least two institutions (one local, one global-accessible).

- Keep emergency funds in a multi-currency wallet like Wise.

4. Inaccessible Customer Service in Emergencies

Many traditional banks operate during fixed business hours in their home country. If you’re halfway across the world and face urgent issues, you may find yourself waiting 24+ hours for a response—or worse, dealing with a chatbot that can’t help.

What You Can Do:

- Test your bank’s international support before you need it. Call or chat from overseas.

- Choose services with 24/7 live support (Wise, Revolut, and some online-only banks).

- Keep screenshots and records of all transactions as evidence if disputes arise.

5. Lack of Multi-Currency Management

Traditional bank accounts are built for domestic use. If you frequently deal with multiple currencies, you may end up paying fees just to hold or convert money.

Example: You receive 2,000 EUR into your USD account. The bank auto-converts it to USD—at a poor rate—and charges a 3% spread.

What You Can Do:

- Open a multi-currency account with platforms like Wise, Revolut, or Payoneer.

- Hold balances in several currencies and convert when rates are favorable.

- Use virtual cards tied to each currency wallet for precise control.

Bonus Trap: Inactivity Fees

Some international or online banks penalize you for not using your account regularly. This is especially common in expat scenarios, where you might only use an account during travel or summer months.

What You Can Do:

- Check for inactivity fees in the fine print.

- Set up automated small transactions to avoid penalties.

- Close unused accounts to avoid unnecessary charges.

Final Checklist – Avoiding the 5 Global Banking Traps

| Trap | Solution |

|---|---|

| Currency Conversion Fees | Compare rates, use fintech tools |

| ATM Withdrawal Charges | Use global ATM-friendly cards |

| Account Freezes | Notify bank, diversify, use 2FA |

| Poor Customer Support | Choose 24/7 fintech platforms |

| Multi-Currency Penalties | Use dedicated wallets for each currency |

Conclusion: Be Proactive, Not Reactive

International banking in 2025 doesn’t have to be complicated—or costly. But the banks aren’t going to warn you.

By understanding the traps ahead of time and switching to smarter alternatives, you can travel, work, and manage money across borders with confidence.