Part 2 — Pick Global Policies Like a Broker

Why this matters

Paying for “coverage” that won’t respond is the most expensive mistake a freelancer can make. This guide teaches you to read policies like a broker, compare apples to apples across carriers, fix gaps with endorsements, and negotiate the few lines that decide whether a claim gets paid. The goal isn’t to become an underwriter; it’s to buy policies that actually respond to the risks you really have—across borders.

Plain-English promise: we’ll unpack declarations, exclusions, sub-limits, retroactive dates, war language, and jurisdiction traps—then hand you worksheets and redlines you can paste into emails.

1) How a policy is actually built (and where truth hides)

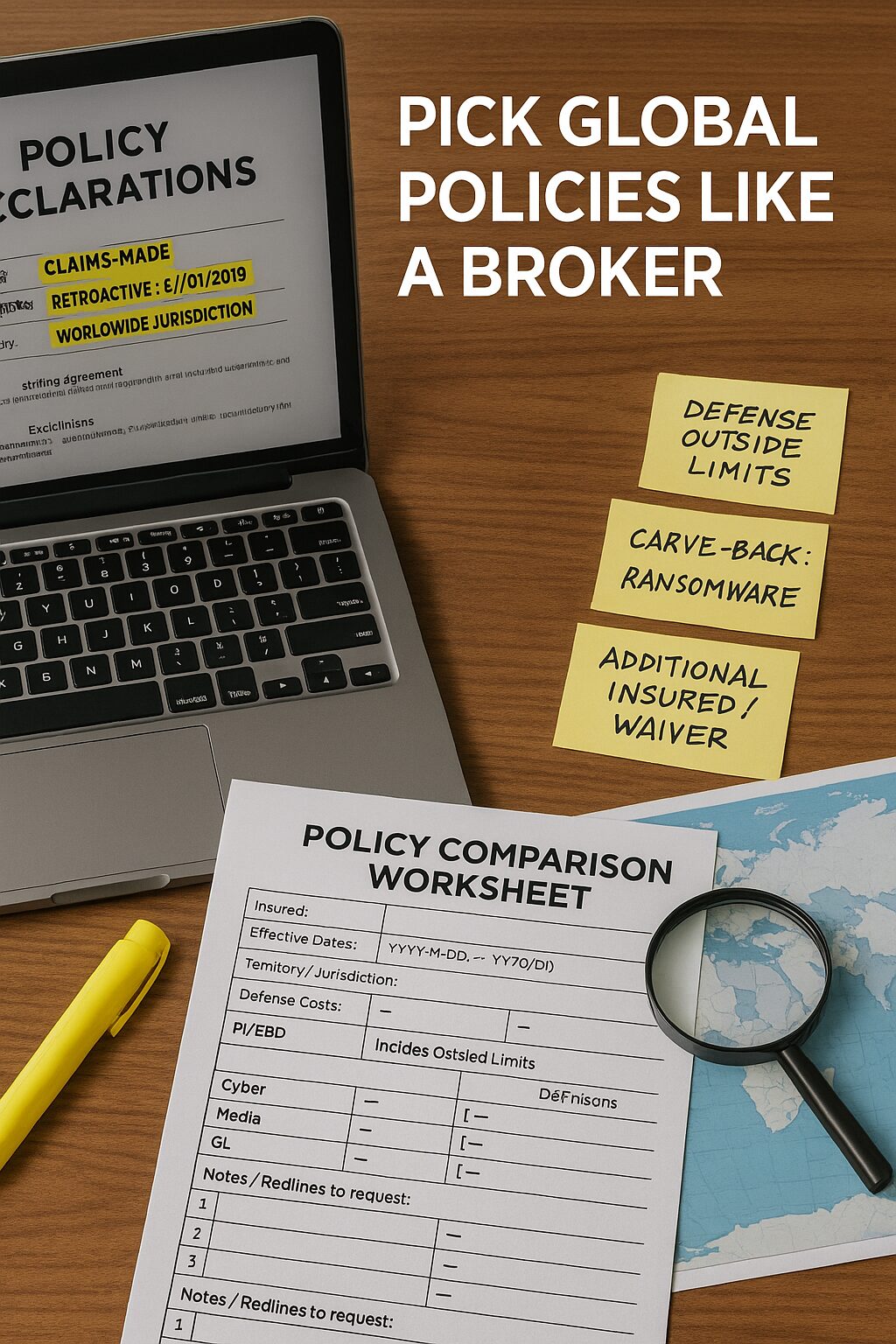

Declarations (Dec Page): who’s insured, limits, deductibles/retentions, retroactive date (if claims-made), territory, policy period, and scheduled endorsements.

Insuring Agreements: the promises—what the carrier will pay for, under what circumstances.

Conditions: duties after a loss, cooperation, notice requirements, consent to settle.

Exclusions: the carve-outs (your first stop after the Dec Page).

Endorsements: add-ons that modify everything above (often the real coverage).

Definitions: the legal meanings of loaded words like “claim,” “loss,” “media content,” “computer system.”

Reading rule: Dec Page → Exclusions → Endorsements → Definitions → Insuring Agreements → Conditions. (Yes, exclusions before the promises. You’re buying what’s left after carve-outs.)

2) Claims-made vs. occurrence—timeline truth you can’t ignore

Most PI/E&O and Cyber are claims-made: the claim must be made and reported during the policy period (or ERP/tail) and the alleged error must occur on or after the retroactive date. Occurrence (common in GL) ties coverage to when the event happened.

You must protect:

- Retroactive Date (Prior Acts): Earlier than your oldest client work, or at least the date you started offering that service.

- Continuity: Do not let claims-made coverage lapse; you’ll lose prior acts.

- ERP (Tail): If you must cancel/switch, buy a tail to report late-arriving claims.

One-minute test: On the Dec Page, confirm (1) claims-made, (2) retro date (e.g., “Retroactive Date: 2019-01-01”), (3) reporting window. If you can’t find the retro date, you probably don’t have prior acts.

Broker email (copy/paste):

“Please confirm claims-made PI and Cyber include prior acts from [YYYY-MM-DD] with no gap in continuity if we renew or switch. Quote ERP options (12/24/36 months) with pricing.”

3) Territory vs. jurisdiction—“worldwide” is not worldwide

- Coverage Territory: where losses can occur.

- Jurisdiction / Where Suits May Be Brought: where claims/lawsuits can be filed and still be covered.

Many policies say “Worldwide” territory but exclude US/Canada jurisdiction or specific regulatory venues. Cyber policies may add OFAC/sanctions constraints; some insert cyber war or “hostile acts” exclusions that nuke ransomware.

Checklist to send brokers:

- Confirm worldwide territory and worldwide jurisdiction including US/CA if you sell there.

- Confirm media/IP is covered worldwide (not only in the country of domicile).

- Ask if the policy is admitted/non-admitted in countries where you’ll spend long stretches.

Redline (paste to broker):

“Endorse territory/jurisdiction to Worldwide including suits brought in US/Canada. Add explicit carve-back for ransomware and data extortion under any war/hostile acts exclusion.”

4) Limits, aggregates, deductibles, sub-limits, and defense costs

- Per Claim / Aggregate: e.g., “$1M each claim / $2M aggregate.”

- Shared Limits: Media + PI sharing one bucket? Dangerous for content/ads.

- Defense Inside vs. Outside Limits: If inside, legal fees erode your limit.

- Sub-limits: social engineering $50k? PCI $25k? Forensics $100k? These matter.

- Waiting periods (BI): 8–24 hours before business interruption triggers.

- Retention/Deductible: Choose what you can pay out-of-pocket without pain.

Heuristics (not advice):

- PI/E&O: 1–2× your largest contract value (start at $1M).

- Cyber: at least the cost of a breach team + a week of revenue; $500k–$1M is a realistic floor for solo operators with access to prod or PII.

- Media: separate $1M if you publish or buy paid media at scale.

- GL: typical vendor minimum $1M per occurrence / $2M aggregate.

Broker ask: “Quote defense outside limits where available; if not, ensure defense sub-limit is sufficient and not shared with indemnity.”

5) Exclusions that quietly delete your coverage (by policy type)

PI/E&O (professional services):

- Broad contractual liability (indemnities you signed).

- IP exclusion (patent/trademark/copyright).

- Insured vs. insured (disputes among co-insured entities).

- Known circumstances (anything you knew about pre-inception).

- Services not listed in the application (declare your real scope).

Cyber:

- War / hostile acts (seek ransomware carve-back).

- Failure to maintain minimum security controls (MFA, backups).

- Infrastructure/utility outage (cloud down? not covered).

- Voluntary parting/social engineering often sub-limited to peanuts.

- Payment card (PCI) assessments tiny sub-limits.

Media:

- Intentional acts (malice), certain personal injuries, IP carve-outs.

- Advertising on restricted platforms not within definition of “media content.”

GL:

- Professional services exclusion (GL won’t cover errors in your work).

- Contractors/subcontractors exclusions.

Travel Medical / Income Protection:

- Pre-existing conditions, high-risk activities, waiting periods, residency rules.

Broker script:

“Please list major exclusions for PI, Cyber, Media, and GL specific to a one-person [designer/developer/consultant] with global clients. Provide endorsement options to restore coverage for: IP in Media, ransomware under Cyber, subcontractor vicarious liability under PI/GL, and social engineering beyond $50k.”

6) Endorsements that save claims (ask for these by name)

- Additional Insured / Primary & Non-Contributory (GL/Auto): for enterprise vendor forms.

- Waiver of Subrogation: prevents your insurer from chasing the client after a claim.

- Prior Acts / Retro Date Backdating (PI/Cyber): preserves older work.

- Worldwide Jurisdiction Add-On: closes the US/CA gap.

- Media Add-On for Ad Buyers: ensures advertising injury and platform use are in.

- Social Engineering Fraud: raise sub-limits above token amounts.

- Contingent/Dependent Business Interruption (Cyber): if cloud providers go down.

- Subcontractor Coverage / Vicarious Liability: if you hire specialists.

Email to broker:

“Attach endorsements: Additional Insured; Primary & Non-Contributory; Waiver of Subrogation; Worldwide Jurisdiction; Prior Acts from [date]; Media Add-On (advertising injury on platforms); Social Engineering $250k; Dependent BI; Subcontractor vicarious liability.”

7) The 30-minute policy reading routine (repeatable)

- Dec Page scan (5 min): Named insured, limits, retro date, territory, jurisdiction, deductible, endorsements list.

- Exclusions sweep (10 min): PI, Cyber, Media—flag IP, war, social engineering, subcontractors, prior knowledge, platform-specific holes.

- Endorsements check (8 min): Do the fixes exist? Note gaps.

- Definitions (5 min): “computer system,” “media content,” “claim,” “loss.”

- Insuring Agreements & Conditions (2 min): confirm notice/reporting duties.

Save findings to your Policy Comparison Worksheet (below).

8) Policy Comparison Worksheet (paste into your doc)

Insured: [Your Name / Company]

Effective Dates: [YYYY-MM-DD to YYYY-MM-DD]

Retroactive Date (PI/Cyber): [YYYY-MM-DD]

Territory / Jurisdiction: [Worldwide / Worldwide incl. US/CA]

Defense Costs: [Inside / Outside Limits]

PI/E&O

- Limit (Each/Aggregate): [ ] / [ ]

- Deductible: [ ]

- Services covered (exact wording): [ ]

- Key exclusions flagged: [ ]

- Endorsements present: Prior Acts [Y/N], Subcontractors [Y/N], IP carve-back [Y/N]

Cyber

- Limit (Each/Aggregate): [ ] / [ ]

- Business Interruption (limit + waiting period): [ ] / [ ]

- Forensics/Legal/PR sub-limits: [ ]

- Social Engineering sub-limit: [ ]

- War/Hostile Acts carve-back for ransomware: [Y/N]

- Dependent BI (Cloud providers): [Y/N, limit]

Media

- Limit (separate or shared?): [ ]

- Platforms included (definition breadth): [ ]

- IP exclusions / carve-backs: [ ]

GL

- Per Occurrence / Aggregate: [ ] / [ ]

- Additional Insured / Primary & Non-Contributory / Waiver: [Y/N]

- Professional services exclusion noted: [Y/N]

Notes / Redlines to request:

- [ ]

- [ ]

- [ ]

9) Ready-to-send broker emails & redlines

A) Line-item quote + fixes

Subject: Global Freelancer — Quote w/ Required Endorsements

Hi [Name],

Please quote PI/E&O ($1M/$2M), Cyber ($1M), Media ($1M separate), GL ($1M/$2M).

Confirm: Worldwide territory and jurisdiction including US/CA, prior acts from [date], defense outside limits where available.

Endorsements required: Additional Insured; Primary & Non-Contributory; Waiver of Subrogation; Social Engineering $250k; Dependent BI; Subcontractor vicarious liability; Media advertising injury on platforms; cyber war exclusion carve-back for ransomware.

Attached: services breakdown, revenue, security controls, claims history (none).

Thanks, [You]

B) Cyber war carve-back language (concept)

“Notwithstanding any war/hostile acts exclusion, this policy shall respond to ransomware, data extortion, and malicious software events not attributable to a nation-state as a formal act of war; ambiguity construed in favor of coverage.”

C) Subcontractor coverage

“Insured includes liability arising out of work performed on the insured’s behalf by independent contractors, provided such work falls under insured services.”

D) Social engineering

“Increase social engineering/funds transfer fraud sub-limit to $250,000 with no requirement that the client first pursue recovery from their bank.”

Use “concept” language with your broker; they’ll map it to carrier-specific wording.

10) Proof pack & COI variations for enterprise onboarding

Keep these ready so new vendor forms don’t stall your contract:

- COI (Certificate of Insurance) listing the client as certificate holder.

- Additional Insured and Primary & Non-Contributory endorsements when asked.

- Waiver of Subrogation endorsement if required.

- Umbrella/Excess schedule if you stack limits above primary.

- One-page Insurance Summary (policy types, limits, retro date, endorsements) with policy numbers redacted.

Email to broker (COI fast):

“Please issue a COI naming [Client Legal Name, Address]. Requirements attached: GL $1M/$2M; PI $1M; Cyber $1M; Additional Insured; Primary & Non-Contributory; Waiver of Subrogation. Due [date].”

11) Decision matrix by freelancer profile (what to prioritize)

Designer/Content/Paid Media: Separate Media $1M (do not share with PI), platform usage inside definitions, ad injury covered; PI lists “creative and advertising services.”

Developer/Automation/Data: Tech E&O with code/integration explicitly named; Cyber BI + Dependent BI; subcontractors endorsed; jurisdiction worldwide incl. US/CA.

Consultant (marketing/RevOps/finance): PI’s “advisory services” wording broad enough; Cyber for access to client systems; GL for workshops/events; social engineering sub-limit raised.

Creator/Photographer/Videographer: Equipment (worldwide, in transit); GL for locations; Media for releases/IP; Travel Medical.

12) Renewal leverage (keep premiums sane)

- Loss runs 30–60 days early; shop market with the same worksheet.

- Document security controls (MFA, backups, EDR) to earn cyber credits.

- Show contract language that limits liability (cap at fees) to reduce PI pricing.

- Bundle lines where it helps, but avoid dangerous shared limits (e.g., Media+PI in one small bucket if you publish heavily).

- Move deductibles up only to the level you can comfortably self-insure.

13) Quick sizing heuristics & self-checks

- Limit heuristic #1: 2× your largest single-client exposure or 6× monthly revenue (pick the higher).

- Deductible test: Could you wire it within 48 hours without derailing payroll/rent?

- BI waiting period: Shorter costs more; choose the longest you can survive with cash reserves.

- Retro date: Should predate your oldest still-used deliverables or code.

- Jurisdiction: If you ever sign US-law MSAs, you need US jurisdiction on policies.

14) Your output from this article (deliverables)

- Completed Policy Comparison Worksheet (one per carrier).

- Redline Pack (copy block of required endorsements).

- Broker Emails (quote + COI scripts).

- Insurance Summary PDF (for vendor onboarding).

Save them in your /Insurance_&_Certificates/ folder and set 60/30/15-day renewal reminders.

Conclusion: Buy outcomes, not buzzwords

Policies aren’t equal. Two documents with the same limit can behave completely differently at claim time. Read the Dec Page. Hunt exclusions. Add endorsements. Lock jurisdiction. Protect your retro date. That’s how you stop paying for air—and start buying responses that pay you back when it counts.

English Case List

- Case: Worldwide—but Not Really — Consultant denied defense because jurisdiction excluded US/CA; added worldwide jurisdiction endorsement on renewal and passed the next vendor audit.

- Case: Retro Date Rescue — Developer switched carriers and almost lost prior acts; broker backdated retro date to the first year of code deployment and added a 24-month ERP.

- Case: Cyber War Trap — Ransomware flagged under hostile acts; carrier honored claim after endorsement added a carve-back for data extortion events not tied to declared war.

- Case: Shared Limits, Empty Bucket — Content studio burned through PI/Media defense inside limits during a takedown dispute; moved to defense outside limits and separated Media $1M.

- Case: Social Engineering Reality — Funds transfer fraud covered only up to $25k; negotiated a $250k sub-limit and client bank-auth process to prevent repeat loss.

Next Article Preview

Part 3 — Client-Mandated Insurance & Certificates (COI) Without Tears.

Enterprise deals die on paperwork, not performance. In the next article you’ll get the COI playbook: how to read vendor insurance requirements, map them to your policies, request endorsements, and issue certificate variants in 24 hours. We’ll include a COI email template pack, a requirement-to-coverage crosswalk, and a same-day checklist so compliance never blocks revenue again. Skip it, and you’ll keep losing weeks—and deals—to forms you could have cleared in a day.