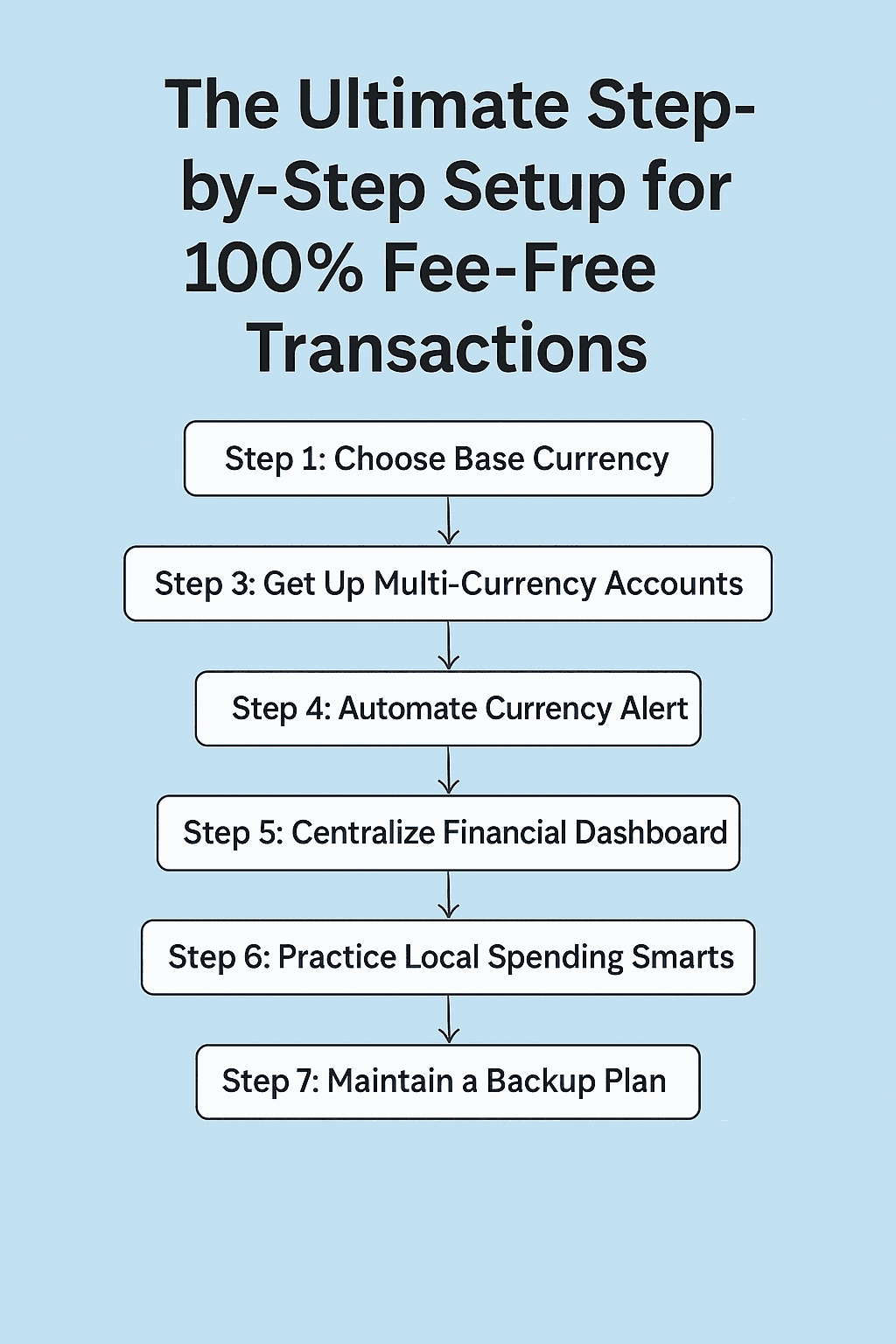

When sending money abroad or paying in a foreign currency, it’s easy to assume the total cost is simply the amount you send or spend. But lurking behind these transactions are invisible fees that quietly chip away at your money—often without you even realizing it.

Let’s break down the most common hidden fees and how to completely avoid them in 2025 and beyond.

1. Currency Conversion Markups

Banks and credit cards often add a hidden margin to the exchange rate—typically 2% to 5%. This is not clearly stated and is buried within the exchange rate itself.

Example: The real rate (mid-market) is 1 USD = 1,300 KRW, but you’re charged 1,260 KRW. That’s a 3% hidden loss.

Solution: Always check mid-market rates on platforms like XE.com or Google and compare with your provider’s rate.

2. Dynamic Currency Conversion (DCC)

When you’re abroad and the payment terminal asks, “Pay in your home currency?”, say no.

DCC lets local merchants charge you in your home currency, but at terrible exchange rates and with extra fees.

Solution: Always choose to pay in the local currency.

3. Foreign Transaction Fees

Many traditional banks still charge 1% to 3% on top of every foreign purchase or withdrawal.

These are pure profit for the bank.

Solution: Use fintech cards like Wise, Revolut, or Charles Schwab which offer 0% fees on foreign transactions.

4. International ATM Fees

These include ATM owner fees, network fees, and possibly your home bank’s fees. They add up quickly—especially on small withdrawals.

Solution: Use global-friendly debit cards that refund ATM fees (e.g., Charles Schwab in the US).

5. Hidden Transfer Fees

Some money transfer services advertise “zero fees” but hide costs in poor exchange rates.

Solution: Use services that are transparent with both exchange rate and transfer fees. Wise and CurrencyFair are excellent examples.

Final Tip: Track Every Fee

Use apps that show real-time fee breakdowns and multi-currency balance tracking. If your provider doesn’t show all fees clearly, switch.

Conclusion

Hidden fees are like silent thieves stealing your money a few percent at a time. In a year, that could mean hundreds of dollars lost. By switching to transparent fintech tools and smart payment habits, you can eliminate nearly all unnecessary costs.