The Complete Blueprint for Building Borderless, Tax-Efficient Wealth

Why You Need a Mastermap

Tax optimization is not a one-step move. It’s a multi-layer architecture — residency, structure, compliance, and lifestyle working together in harmony.

Most people try to minimize taxes without realizing that residency drives everything: your banking options, your access to investment vehicles, even how you’re taxed on dividends or digital income.

This Mastermap exists to connect all parts of the puzzle.

Each article in this series builds upon the previous one — from understanding your tax base to designing multi-residency systems and integrating your entire life into one lawful, global framework.

Whether you are a remote founder, investor, or family office executive, this blueprint is your reference point for creating borderless, compliant, and tax-efficient wealth.

The Six Foundations of Global Residency & Tax Planning

The complete series unfolds across six interconnected stages.

Each part represents one essential layer in your global wealth system.

Part 1 — Why Residency Drives Tax Outcomes

Residency is not where you live — it’s where your wealth legally exists.

- Learn the core differences between citizenship, residency, and tax domicile.

- Understand how the wealthy legally lower their tax obligations through strategic relocation.

- Identify key signals that it’s time to move your tax base — lifestyle friction, dual reporting burdens, or capital flow restrictions.

Read here → Why Residency Drives Tax Outcomes

Core Insight:

Residency is the foundation of every tax decision. Without defining your base, no offshore plan or structure will stand securely.

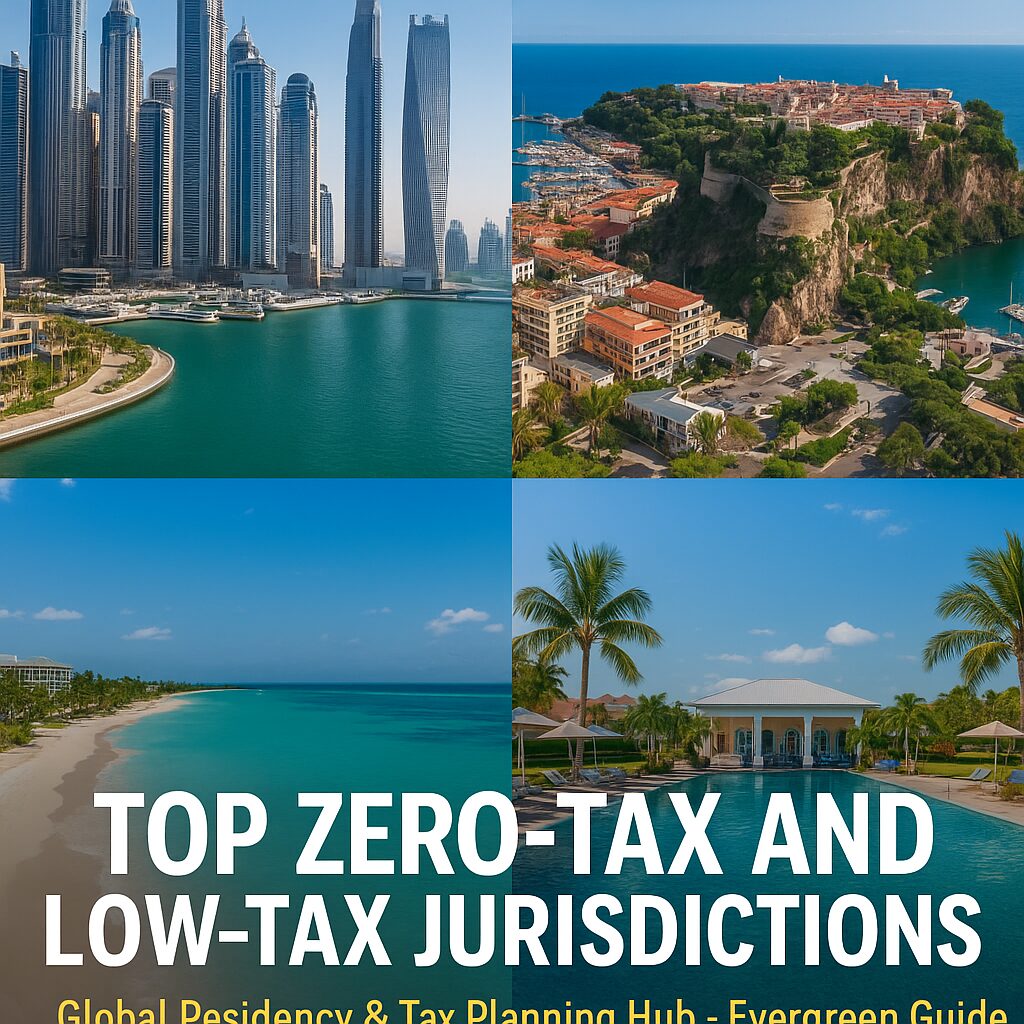

Part 2 — Top “Zero-Tax” or “Low-Tax” Jurisdictions

When less tax means more control — and more responsibility.

Explore the world’s most famous low-tax jurisdictions:

Dubai, Monaco, Cayman Islands, Bahamas, and Vanuatu.

Each offers freedom, but each has trade-offs:

cost of living, substance requirements, lifestyle culture, and exit barriers.

Read here → Top Zero-Tax or Low-Tax Jurisdictions

Core Insight:

Zero tax doesn’t mean zero complexity.

A jurisdiction with no tax may still demand physical presence, audits, or strict banking compliance.

Part 3 — Best “Moderate Tax but High Treaty” Countries

Sometimes paying a little tax opens big doors.

Some countries strike a balance between low rates and legal credibility:

Portugal (NHR), Spain (Beckham Law), Ireland, and Singapore.

Learn why paying a moderate rate with strong treaty benefits often beats chasing zero-tax status — especially for entrepreneurs, remote founders, and nomad families.

Read here → Best Moderate-Tax but High-Treaty Countries

Core Insight:

Moderate tax nations often give you better access to banking, credit, and investment protection — with fewer compliance risks.

Part 4 — Multi-Residency & Second Citizenship Strategies

Why one residency is never enough.

The ultra-wealthy diversify their residencies just like assets.

This article teaches how to stack residencies to access multiple markets —

using Golden Visas, Start-up Visas, or naturalization programs.

Mini-cases show investors holding three residencies and one second passport, creating unmatched mobility and diversification.

Read here → Multi-Residency & Second Citizenship Strategies

Core Insight:

Freedom is optionality.

Residency stacking gives you tax flexibility, visa mobility, and jurisdictional leverage — without renouncing your citizenship.

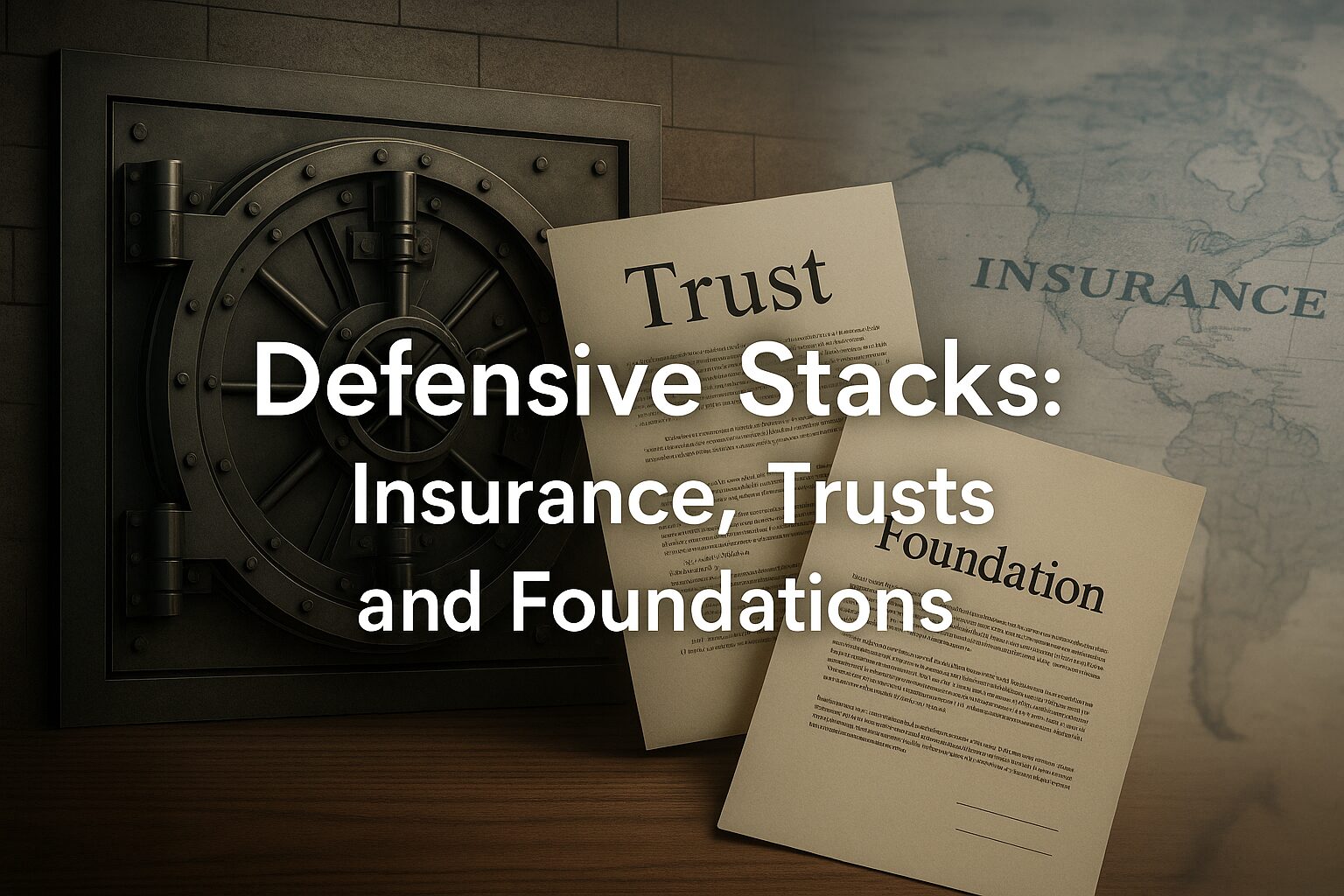

Part 5 — Tax Optimization Tools Without Moving

When relocation isn’t possible, structure does the job.

Learn how to use offshore companies, trusts, and insurance wrappers

to achieve tax efficiency while staying in your home country.

You’ll discover the right balance between physical mobility and structural mobility —

ensuring your income flows are legally optimized.

Read here → Tax Optimization Tools Without Moving

Core Insight:Start Here

Not everyone needs to relocate.

A well-structured offshore entity or compliant trust can achieve near-identical results — if done transparently and lawfully.

Part 6 — The Hidden Architecture of Global Wealth

How lifestyle, protection, and compliance form one living system.

This final article reveals how the global elite synchronize their lifestyle, asset protection, and compliance systems into one coherent framework.

From multi-jurisdiction banking and healthcare to family governance and education planning, it’s the invisible design behind sustainable global wealth.

Read here → The Hidden Architecture of Global Wealth

Core Insight:

The true advantage of wealth is not hiding it — it’s engineering it lawfully across compliant, interconnected jurisdictions.

How to Use This Mastermap

This Mastermap is more than a reading index — it’s your global wealth operating manual.

Here’s how to use it:

Read sequentially: Start from Part 1 to 6 to understand the logic of tax-driven residency design.

Apply interactively: Use each internal link as a workflow — audit your own structure part by part.

Build your stack: Combine your preferred jurisdictions, structures, and compliance tools.

Cross-reference: Each article includes checklists and mini-cases — replicate the framework that matches your profile.

Stay evergreen: No time-sensitive laws or deadlines — this knowledge remains valid across years and economic cycles.

The Global Residency & Tax Framework (Visual Overview)

Layer 1: Residency Base

Where you live, pay tax, and hold your primary documentation.

Layer 2: Structural Shell

Companies, trusts, or foundations controlling assets.

Layer 3: Compliance Core

Substance, CRS alignment, and transparent reporting.

Layer 4: Lifestyle Integration

Banking, schooling, healthcare, and property tied to your residency.

Layer 5: Wealth Governance

Family office management, succession planning, and investment controls.

Together, these layers form the architecture of borderless wealth — clean, legal, and profitable.

The Compounding Effect of Global Compliance

The wealthiest families treat compliance as leverage.

They file early, declare clearly, and structure intentionally.

Instead of hiding assets, they design ownership transparency that protects them across jurisdictions.

Banks open faster, audits close cleaner, and investments compound quietly — without legal risk.

The longer your structure stays compliant,

the more valuable it becomes — like compound interest for legitimacy.

Key Takeaways from the Series

| Area | Core Lesson | Result |

|---|---|---|

| Residency | Drives taxation & mobility | Legal flexibility |

| Jurisdiction | Each offers unique trade-offs | Portfolio diversification |

| Multi-Residency | Layered freedom | Access to global systems |

| Offshore Tools | Legal efficiency | Lower burden, higher yield |

| Lifestyle Integration | Stability & trust | Seamless global living |

| Compliance | The hidden ROI | Peace of mind & longevity |

Downloadable Checklist (Lead Magnet)

“Global Residency & Tax Planning Checklist — Build Your Own Map”

Download your personal residency planning template:

- Residency vs Domicile Diagnostic

- Jurisdiction Comparison Grid

- Offshore Structure Readiness Test

- Annual Compliance Calendar

(Insert CTA button: “Download the Checklist (PDF)”)

This turns readers into subscribers — feeding your email funnel + AdSense engagement simultaneously.

Internal Link Map (SEO Engine)

| Page | Purpose |

|---|---|

| Part 1 → Hub | Foundational entry keyword “Tax Residency Meaning” |

| Part 2 → Hub | High CPC keyword “Zero Tax Jurisdictions” |

| Part 3 → Hub | Moderate Tax / Treaty SEO cluster |

| Part 4 → Hub | Second Citizenship traffic funnel |

| Part 5 → Hub | Offshore Company / Trust traffic cluster |

| Part 6 → Hub | Lifestyle & Compliance + Authority Signal |

| Hub → All | High retention loop and “evergreen pillar” page |

All internal links create a closed SEO loop — multiplying traffic between parts and boosting domain authority.

Conclusion — The Mastermap Mindset

True wealth isn’t earned; it’s architected.

By aligning your residencies, jurisdictions, and compliance systems,

you create a life where freedom, legality, and profitability reinforce each other.

Every border, every rule, every treaty — becomes part of your design.

You are not escaping the system; you’re mastering it.

This is the ultimate mindset of the global elite:

freedom through structure, power through compliance.

Subscribe CTA

Knowledge becomes wealth only when applied.

Join our community of global citizens designing tax-efficient, borderless lives.

Subscribe to HealthInKorea365 for exclusive blueprints, residency breakdowns, and advanced compliance insights.

Your next level of freedom starts here.