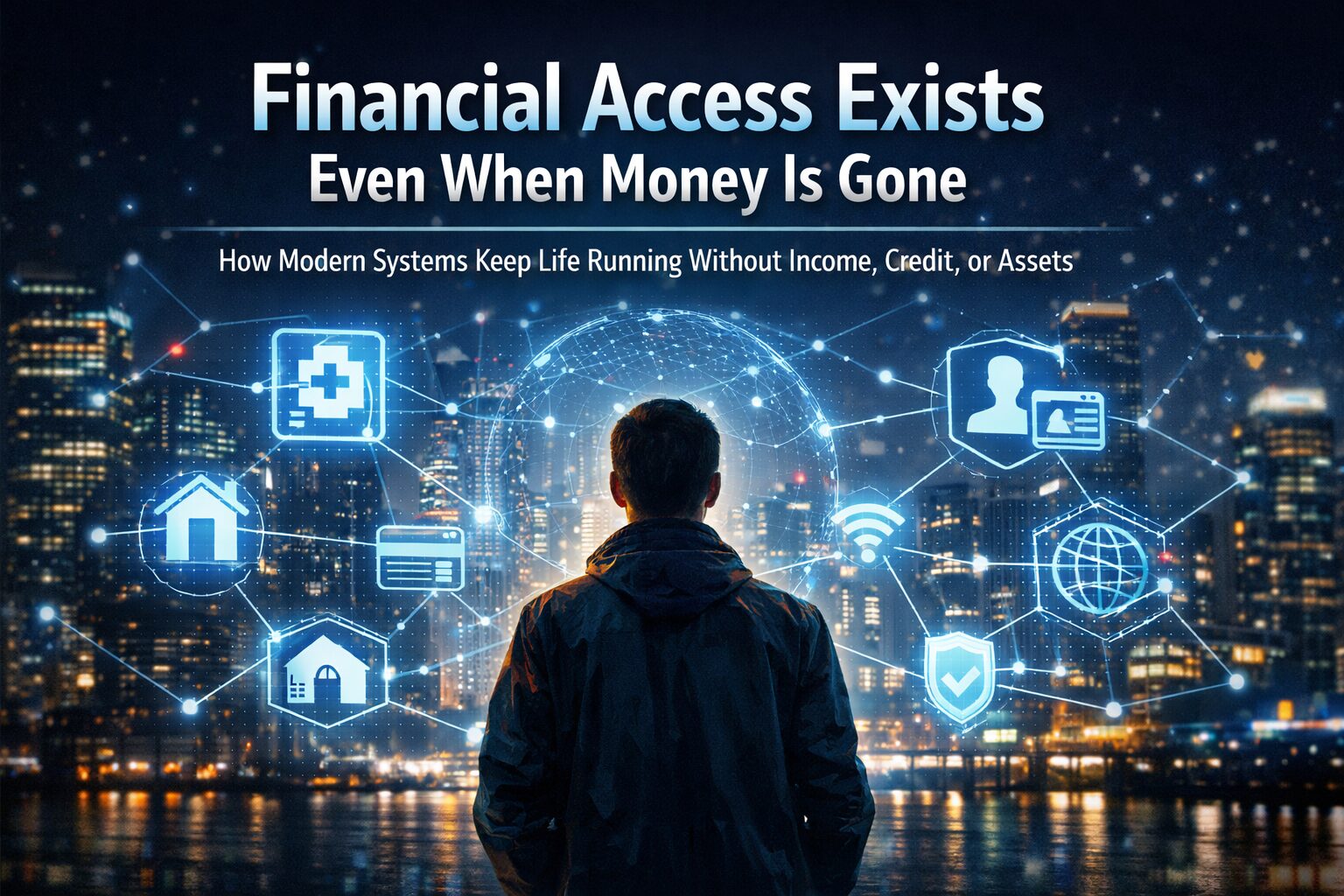

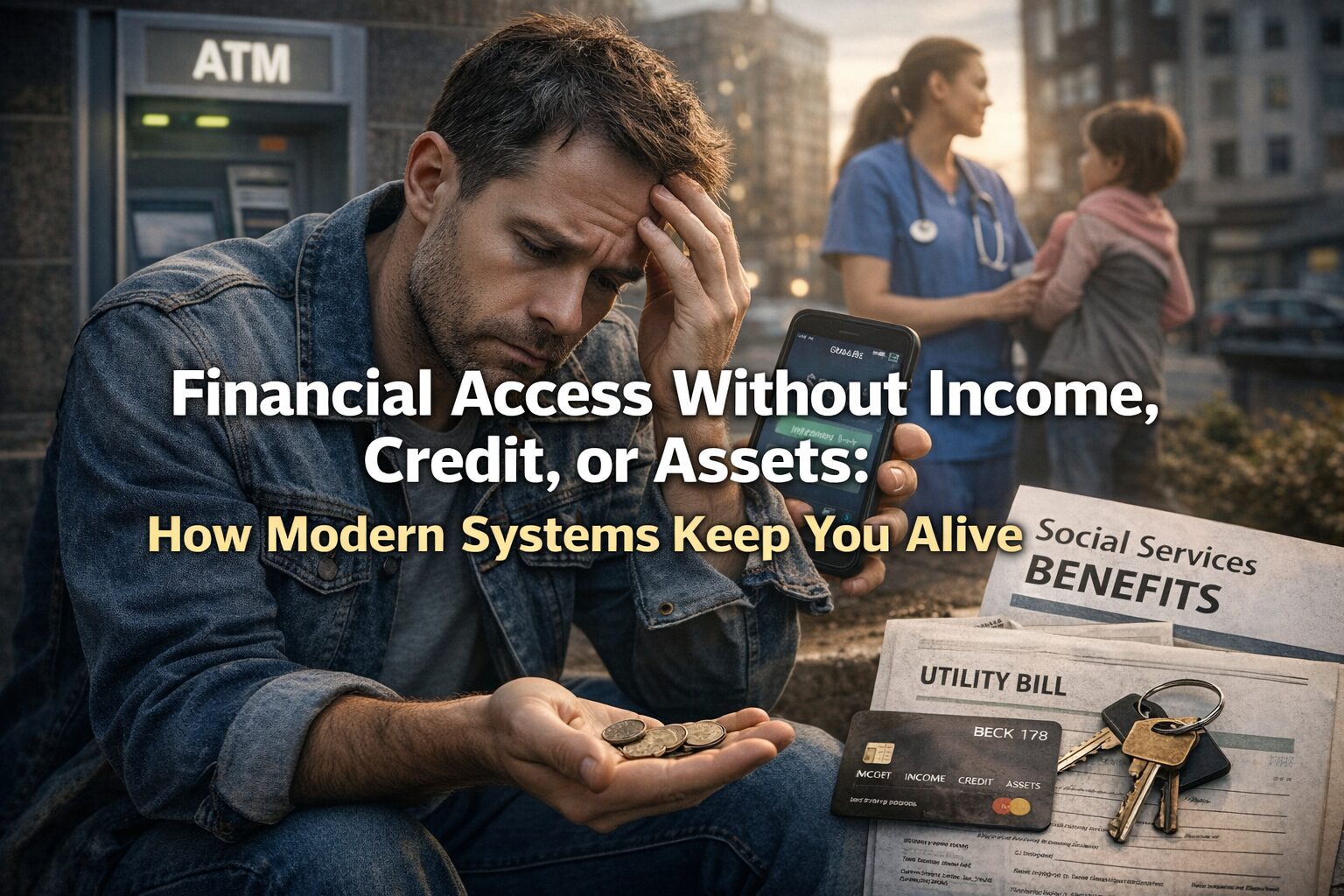

Most people believe that financial access depends on three things: income, credit, and assets.

Lose all three, and life is assumed to collapse.

Bank accounts disappear.

Cards stop working.

Services shut down.

Opportunities vanish.

This belief creates panic.

But modern society does not operate this way.

In reality, financial access is not granted by personal success.

It is maintained by structural systems.

Even when income disappears.

Even when credit weakens.

Even when assets are gone.

You are still connected.

This article explains how that connection works, how to protect it, and how to use it to stabilize your life.

The Hidden Architecture Behind Financial Access

Financial access is not a privilege.

It is infrastructure.

Behind every transaction, account, and service lies a layered system designed to prevent total exclusion.

These layers include:

Identity systems

Banking networks

Government registries

Utility databases

Digital verification platforms

Payment processors

Insurance frameworks

Once you enter these systems, you are rarely removed completely.

Instead, access is downgraded, redirected, or restricted.

But it is almost never erased.

This is intentional.

Societies that cut people off entirely collapse internally.

So modern systems are designed to keep individuals connected at a minimum operational level.

Why Income Is Not the Main Gatekeeper

Income feels powerful, but it is not central.

It only determines how much access you have, not whether you have access.

When income disappears:

Accounts remain open

Basic payment functions stay active

Minimum balances are protected

Essential billing channels continue

Digital wallets remain linked

This happens because banks profit from long-term presence, not short-term activity.

An inactive customer is still a future customer.

Removing you completely destroys future value.

So institutions preserve access.

Credit Is Not Control, It Is Pricing

Credit is often misunderstood.

It does not decide whether you can participate.

It decides how expensive participation becomes.

When credit weakens:

Interest rises

Limits shrink

Options narrow

But access remains.

You can still:

Receive money

Store funds

Pay bills

Transfer assets

Use digital platforms

Credit is a pricing mechanism, not a gate.

Asset Ownership Is Not Required for Participation

Assets create leverage.

They do not create eligibility.

Modern systems operate on identity continuity, not wealth possession.

As long as you exist in official records:

You remain bankable

You remain billable

You remain serviceable

You remain insurable

You remain traceable

These qualities matter more than ownership.

The Core Protection Layer: Identity Continuity

Everything begins with identity.

Your legal and digital identity forms your permanent access key.

This includes:

Government identification

Residency records

Tax registration

Mobile number verification

Biometric links

Platform accounts

As long as these remain intact, financial exclusion is extremely difficult.

Protecting identity continuity is more important than protecting money.

Once identity is stable, access can always be rebuilt.

How Accounts Survive During Financial Decline

Most people fear account closure.

In practice, closure is rare.

Institutions prefer dormancy.

Dormant accounts:

Cost little

Preserve data

Maintain compliance

Enable reactivation

To keep accounts alive:

Maintain minimal activity

Receive small transfers

Keep contact information updated

Respond to system notices

Preserve login access

These simple actions preserve long-term access.

Payment Networks That Never Fully Disconnect

Global payment systems are interconnected.

They rely on participation volume.

Disconnecting users weakens networks.

So they preserve minimal access.

This applies to:

Card networks

Mobile payments

Digital wallets

Remittance platforms

Online banking

Even under restriction, routing paths remain open.

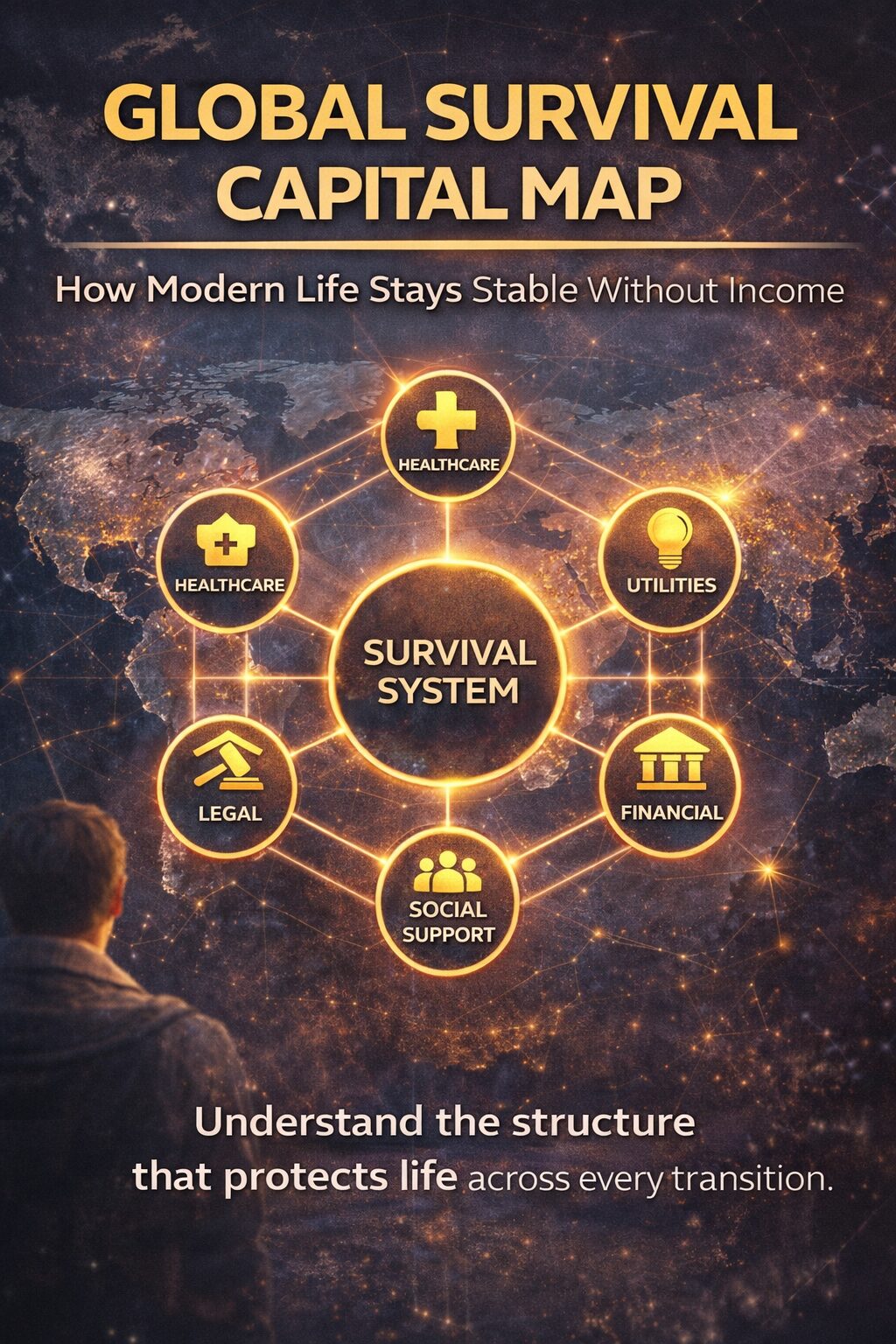

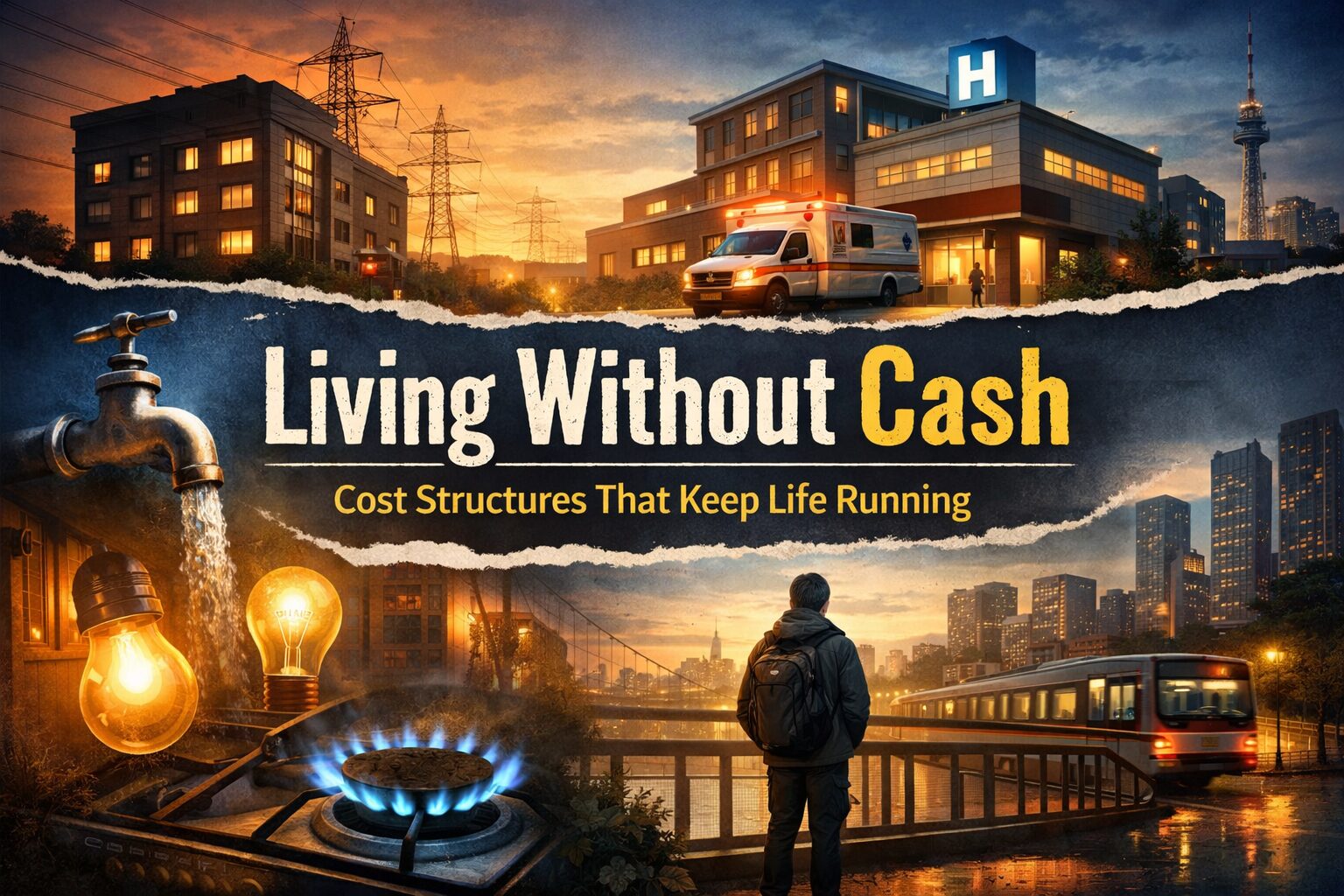

Healthcare, Housing, and Utility Linkages

Essential services are integrated with financial systems.

Healthcare providers, housing authorities, and utilities share verification channels.

This creates continuity.

When income drops:

Medical access continues

Housing contracts remain

Utility supply persists

Billing shifts to flexible structures

Disconnection is avoided because reconnection is costly.

Systems prefer maintenance over removal.

Government Stabilization Mechanisms

Public systems operate as backstops.

They are activated automatically through data signals.

These include:

Employment registries

Health insurance databases

Social contribution records

Local residency systems

Welfare platforms

You do not need perfect status.

Partial presence is enough.

Once registered, you remain visible.

Visibility equals support eligibility.

Digital Platforms as Secondary Financial Anchors

Modern life is platform-based.

Major platforms now function as parallel financial systems.

They provide:

Wallet functions

Payment processing

Identity verification

Transaction histories

Credit scoring inputs

Maintaining platform integrity expands financial resilience.

Never abandon digital presence.

Case Scenario: Income Loss Without System Collapse

A worker loses employment.

Income stops.

Fear rises.

But:

Bank account remains

Medical coverage continues

Rental agreement stands

Mobile payments function

Government records stay active

Access is reduced, not removed.

Stability is maintained.

Case Scenario: Business Shutdown Without Exclusion

A business closes.

Revenue disappears.

Debt remains.

Yet:

Personal accounts stay open

Tax identity remains

Payment tools persist

Credit history continues

Insurance coverage holds

The system allows recovery.

Case Scenario: Long-Term Low Activity

A person enters minimal economic participation.

Few transactions.

Limited income.

Still:

Digital presence remains

Basic services function

Public records persist

Platform accounts stay active

Re-entry is always possible.

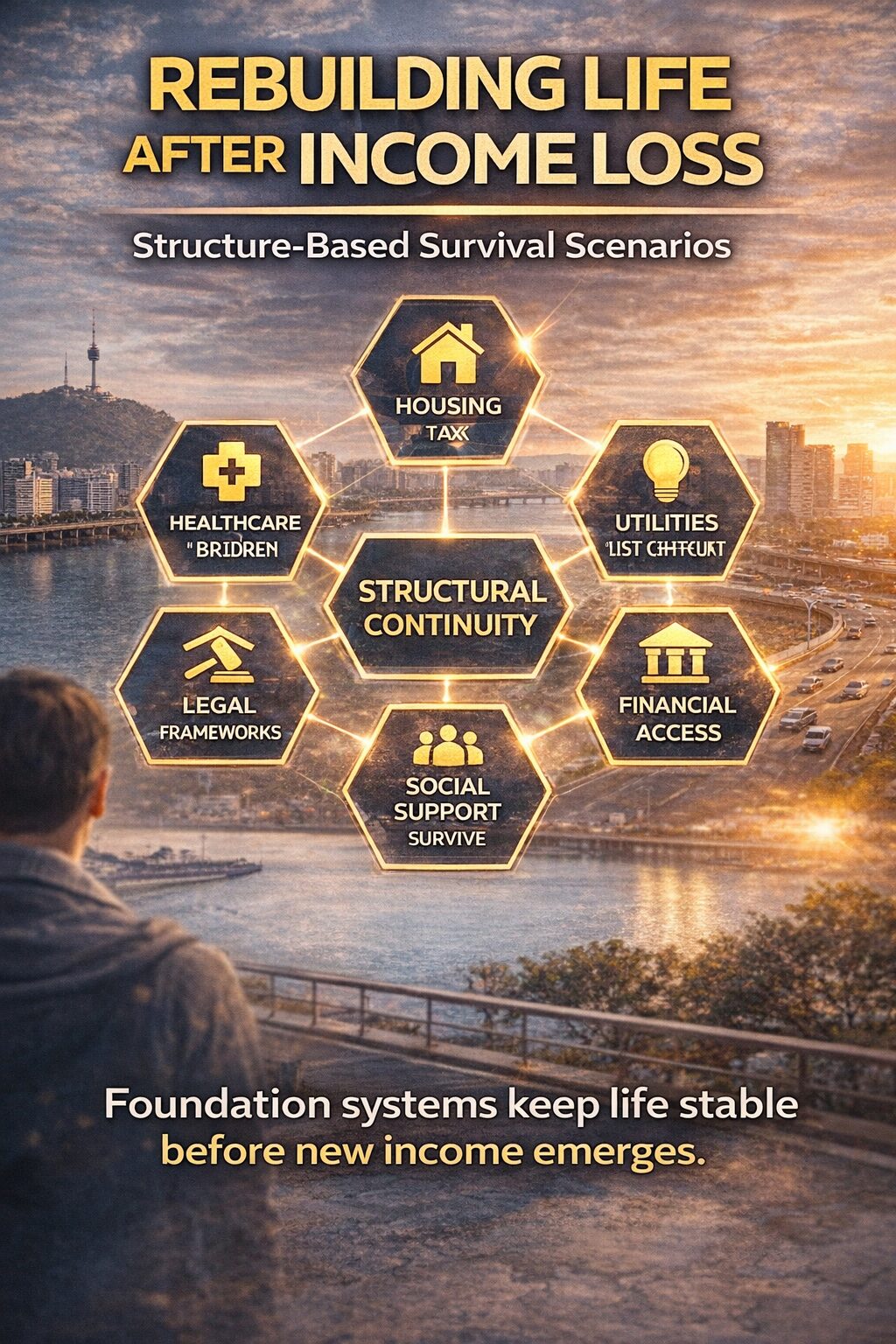

The Survival Access Strategy

To protect and expand financial access, focus on systems, not money.

Maintain Identity

Keep documents valid

Update addresses

Preserve contact channels

Preserve Accounts

Avoid abandonment

Maintain login access

Monitor notices

Protect Digital Footprint

Secure major platforms

Maintain recovery methods

Avoid permanent bans

Stay Visible

File required reports

Maintain registrations

Respond to official messages

Visibility equals continuity.

How to Rebuild Leverage From Minimal Access

Once access is preserved, leverage can be rebuilt.

Through:

Skill monetization

Platform income

Service provision

Digital products

Remote participation

Micro-contracting

Access enables opportunity.

Opportunity enables income.

Income enables expansion.

Why Total Financial Exclusion Is Structurally Avoided

Societies fear disengagement.

Disconnected populations create instability.

So systems are designed to absorb pressure.

Not eliminate participants.

You are part of the system even at your weakest.

The Long-Term Advantage of Structural Awareness

Understanding systems creates advantage.

You stop panicking.

You stop making destructive decisions.

You stop liquidating unnecessarily.

You stop abandoning access points.

You operate strategically.

Conclusion: You Are Inside the System

Financial access is not granted by success.

It is maintained by structure.

As long as your identity exists, your access exists.

As long as access exists, rebuilding is possible.

Stability is structural.

Use it.

Next Article Preview

Reader Continuity Invitation

If this framework changed how you see financial survival, continue through the series to master the complete Global Survival Finance System.

Each article builds a permanent advantage.