From second passports to Golden Visas, tax residency, real case stacks, and a final blueprint you can copy.

Build a stack that actually works under scrutiny: a passport for mobility, a residency you can defend, and banking/company rails partners trust—locked in with an Audit File so reviews stay green. This hub gathers all six long-form guides, each written to be evergreen and directly actionable. Start where you are, then follow the path that fits your life and business.

Series Index (cards)

Use your own permalinks if they differ; below are clean slugs you can keep.

- Top Citizenship by Investment Programs — Caribbean to Europe

How ordinary people (not just billionaires) get real mobility.- Fast Caribbean options vs. prestige EU routes

- Banking perception & due-diligence realities

- Copyable cases and decision matrix

→ Read now:/top-citizenship-by-investment-programs-caribbean-to-europe

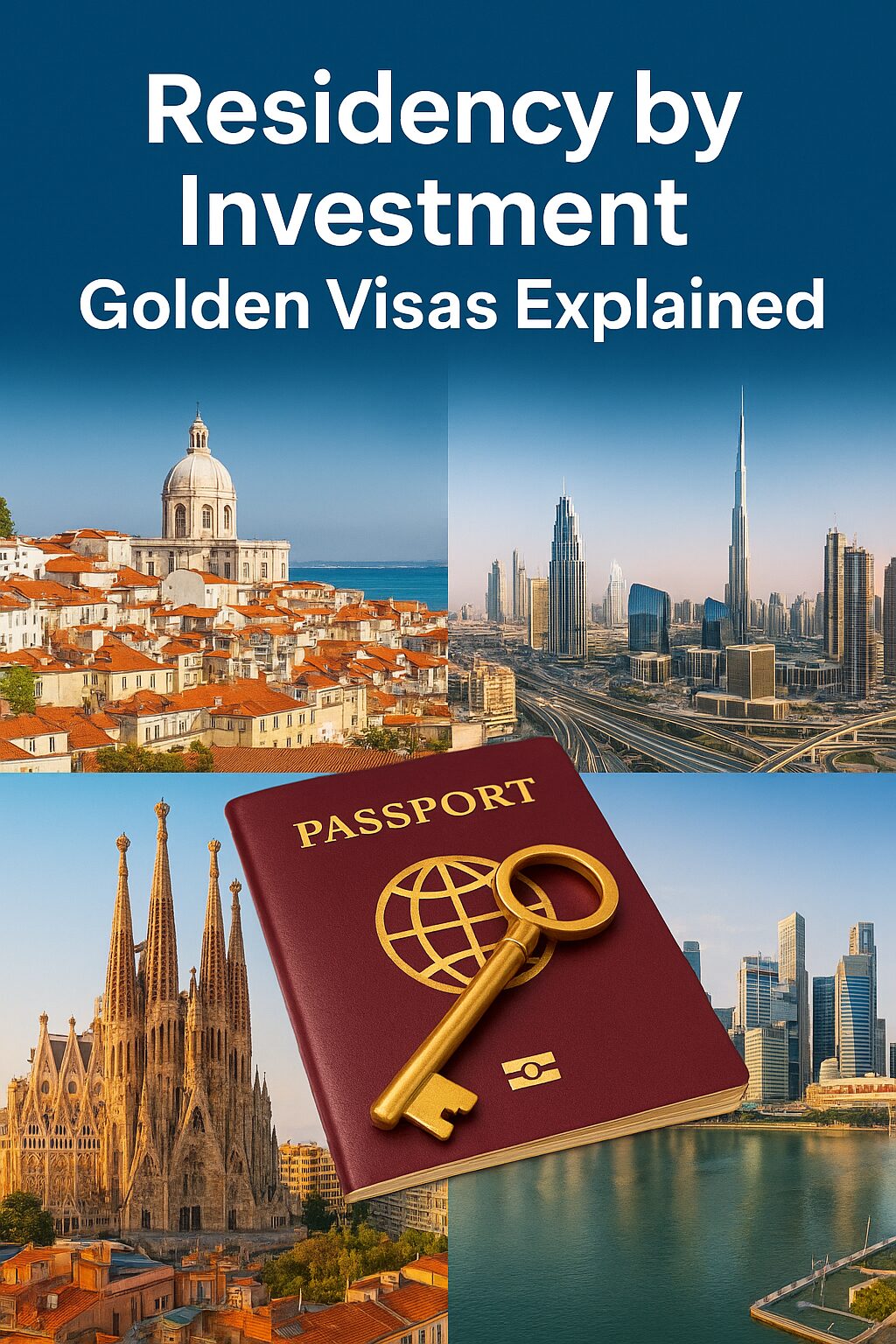

- Residency by Investment — Golden Visas Explained

Why residency is the smarter first step (with success & failure cases).- EU, UAE/Asia options compared

- Minimum stay pitfalls, policy shifts, exit strategies

- Checklist to pick your Golden Visa

→ Read now:/residency-by-investment-golden-visas-explained

- Tax Residency vs. Citizenship — What’s the Difference?

Stop mixing identity with taxation—stay compliant and keep more.- Day-count, center-of-life, treaty tie-breakers

- 12-point change-of-residency checklist

- Audit-proof habits that compound

→ Read now:/tax-residency-vs-citizenship

- Second Passports for Entrepreneurs & Digital Nomads

Mobility tools, not trophies—stacks that remove real bottlenecks.- Founder/nomad use-cases with mini-cases

- Banking acceptance & PSP stability

- Mistakes to avoid (and fixes)

→ Read now:/second-passports-for-entrepreneurs-digital-nomads

- Case Studies — Celebrities, Billionaires, and Global Families

Replicable stacks, step-by-step: what worked, what failed.- Athlete, musician, founder, trader, family patterns

- How to copy on a normal budget

- Risks that trigger audits or freezes

→ Read now:/case-studies-celebrities-billionaires-global-families

- The Final Blueprint — Building Your Multi-Passport Portfolio

The construction manual: layers, milestones, stacks, templates.- Mobility → Residency → Rails → Stability

- Playbooks, decision matrix, PE/KYC templates

- Folder tree for your Audit File

→ Read now:/final-blueprint-multi-passport-portfolio

“Start Here” — Choose Your Path (anchors inside this page)

- Founders (US/EU sales): Read 4 → 3 → 6, optionally 1/2 to add mobility/residency.

- Creators/Nomads: Read 4 → 5 → 6, then 3 for compliance discipline.

- Global Families: Read 2 → 5 → 6, optionally 1 for faster mobility.

- Traders/Crypto: Read 3 → 6 → 5, keep the Audit File routine.

CTA: Not sure where to begin? Start with #6 The Final Blueprint and follow the Milestones.

Downloads & Templates (link to the relevant posts)

- Audit File checklist & folder tree: in #6 The Final Blueprint →

/final-blueprint-multi-passport-portfolio - Residency Narrative one-pager: in #6

- KYC Bundle index + PE memo outline: in #6

- Decision Matrix (scorecard): in #6

FAQ (evergreen)

Q1. Do I need a second passport to change my taxes?

No. Taxes follow residency facts and filings, not citizenship. See #3.

Q2. Should I start with citizenship or residency?

Most readers start with residency (Golden Visa) and add citizenship later. See #2 and #1.

Q3. Will a Golden Visa guarantee profitable real estate?

No—underwrite as if there were no visa. See failure cases in #2 and #5.

Q4. Why do accounts freeze?

Mixed income streams, weak evidence, or single-provider dependency. Fix with stream separation, KYC bundle, and two-region banking. See #4/#5/#6.

Internal Navigation (optional “Next/Prev” at page bottom)

- Previous: n/a (This is the series hub)

- Next: #1 CBI Guide →

/top-citizenship-by-investment-programs-caribbean-to-europe

Build a system, not a souvenir: pick one outcome—mobility, banking reliability, market access, or family stability—and take the first step today; if you’re unsure where to begin, go straight to The Final Blueprint (/final-blueprint-multi-passport-portfolio) or jump into #1 CBI Guide (/top-citizenship-by-investment-programs-caribbean-to-europe), keep your Audit File updated, and let the stack compound freedom and income—quietly, cleanly, and legally.